BONDS FAVORABLE AMID POTENTIAL RECESSION RISKS

Over the past few weeks, volatility in financial markets has surged, as if investors suddenly recognized that the probability of recession in the coming months is greater than zero. The data that has most alarmed investors’ concerns the labour market. In early August, the number of new hires increased less than anticipated, while layoffs of part-time workers exceeded expectations, pushing the unemployment rate to 4.30%. As a result, investors have begun to think that the Fed is late in cutting rates, causing the yield on the two-year Treasury to drop. Specifically, from the end of July, the yield has dropped by 40 basis points, stabilizing in the 4.00% area.

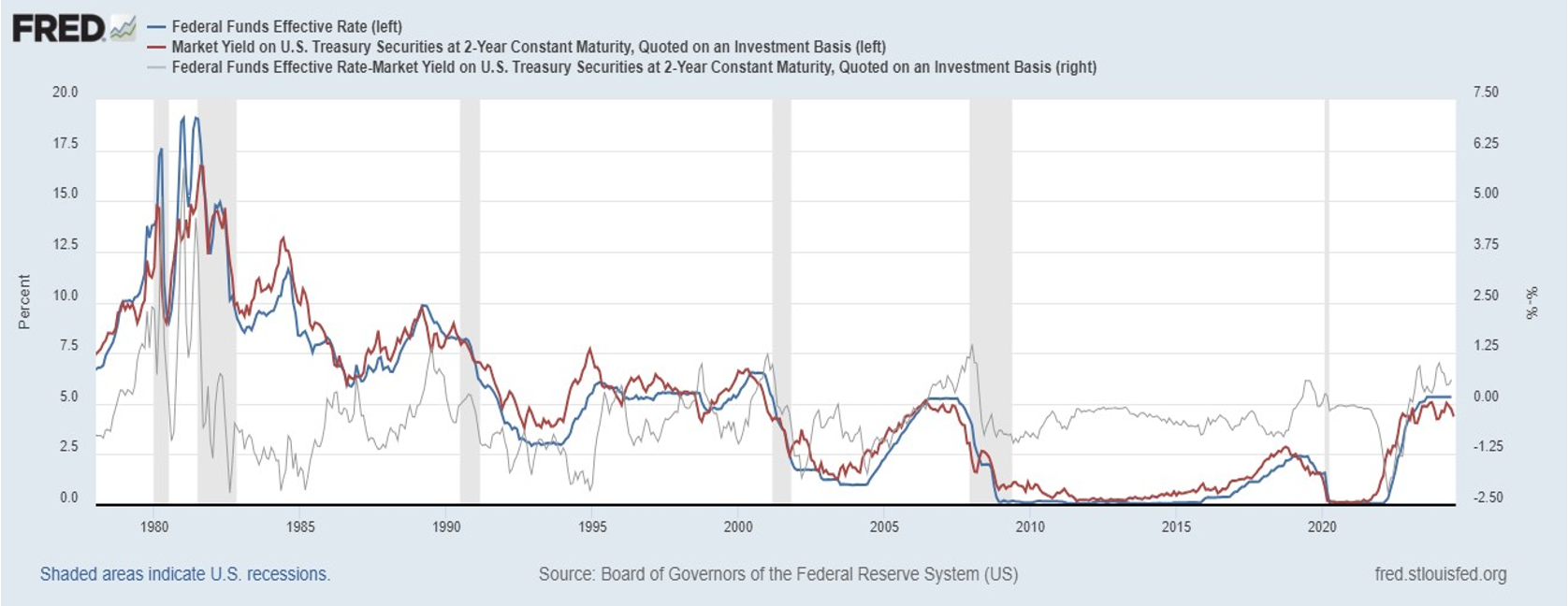

In our study, we analysed historical trends following a rapid decline in the yield on the two-year Treasury, particularly when this yield falls below the rate set by the Fed (see Chart 1). Since the late 1970s, each time this scenario has occurred, the Fed has responded by cutting interest rates, yet it has consistently failed to prevent a subsequent recession. The only exception was between 1995 and 1999, but the chances of a similar outcome today are slim. This could have a significant impact on the stock market.

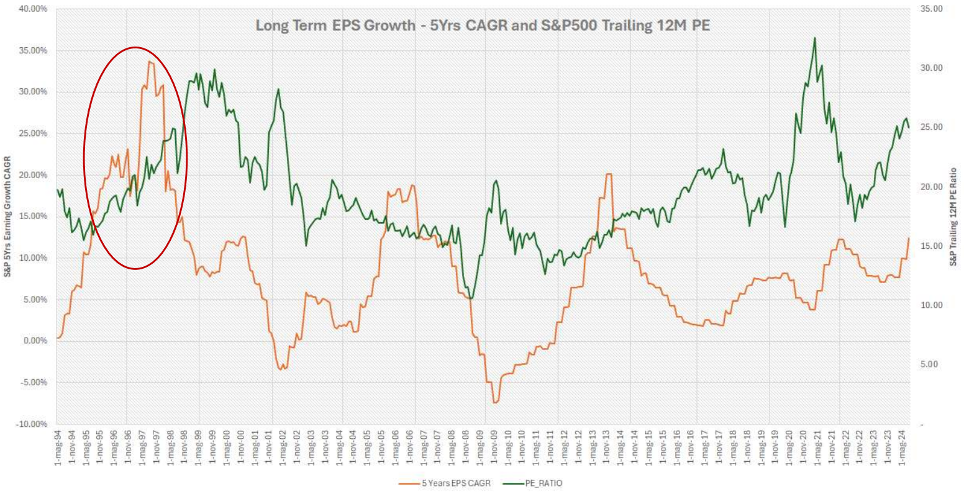

During that five-year period, the equity markets did not decline; instead, It experienced significant growth driven by an expansion in the P/E multiple. As shown in the red-highlighted boxes in Chart 2, the P/E ratio of the S&P 500 rose from around 16 to 30, surpassing the historical average and entering the overvalued zone. Today, we are already within this zone, with the P/E multiple at 29.60. It is unlikely that what we saw in the late 1990s will be repeated.

The primary driver of this stock market movement was the significant increase in expectations for five-year earnings growth (see Chart 3), fuelled by the rise of the Internet and its anticipated benefits. Today, however, it is difficult to foresee a similar surge in expectations due to the advent of Artificial Intelligence, despite the notable jump observed over the past year.

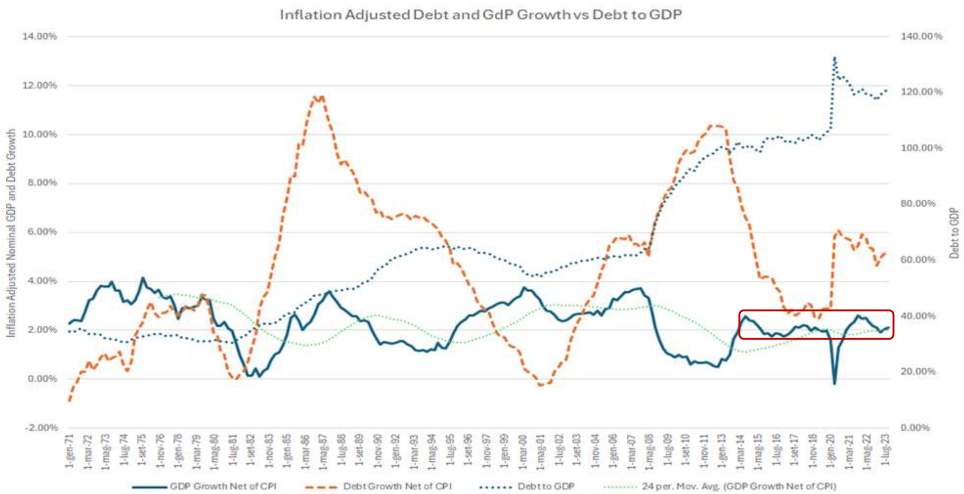

Our scepticism is rooted in the trend of U.S. Real GDP growth over the past decade. As shown in Chart 4, GDP growth Net of CPI (blue line) surged to nearly 4% in the late 1990s. In contrast, over the past ten years, Real GDP growth has been stable around 2%, with increases beyond this level occurring only due to government stimulus.

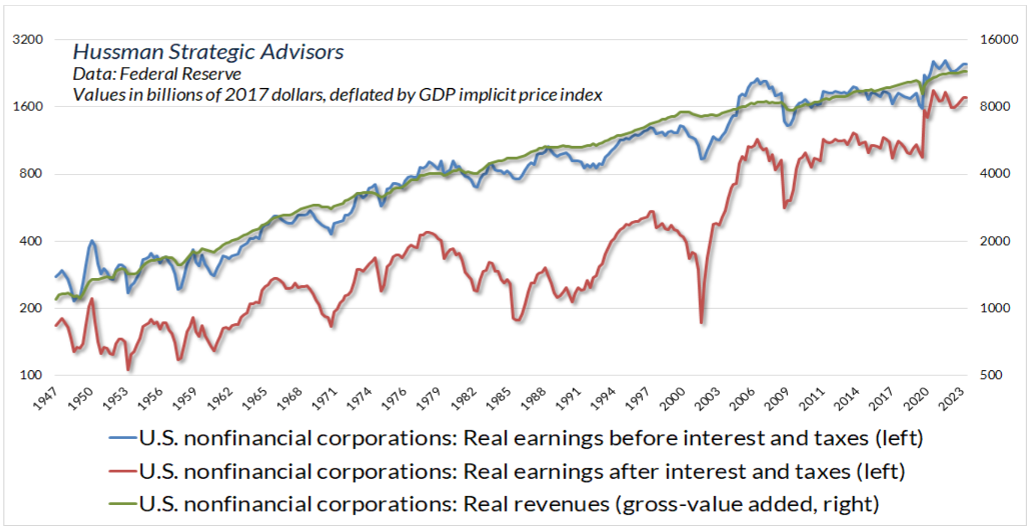

However, such stimulus and aid are unlikely to continue, given the massive deficit run by the U.S. government over the past three years, which has led to a significant increase in total debt. Additionally, it is improbable that growth drivers will include lower interest rates or tax relief. Chart 5 illustrates that the difference between companies' real earnings before and after paying the cost of debt and taxes is at an all-time low, excluding 2020, which was impacted by the COVID-19 pandemic. Higher profit will not benefit, as in the past, by lower interest rates and taxes, the contrary is more likely.

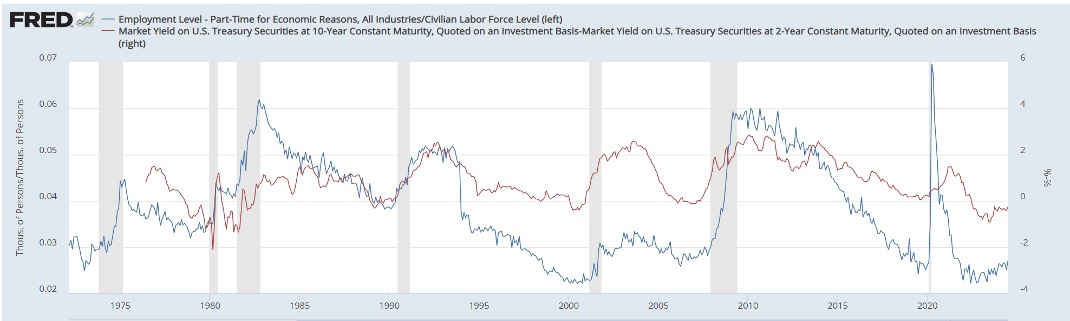

Lastly, when considering the labour market, which, as mentioned earlier, is cooling, we have another factor suggesting that the soft landing of the late 1990s is unlikely to be repeated. Chart 6 shows the increase in the number of part-time workers for economic reasons following the un-inversion of the 10-year/2-year yield curve—an event historically signalling an impending recession. Since the mid-1980s, the average increase in part-time workers has been 0.41%, while the average rise in the unemployment rate has been 1.5%.

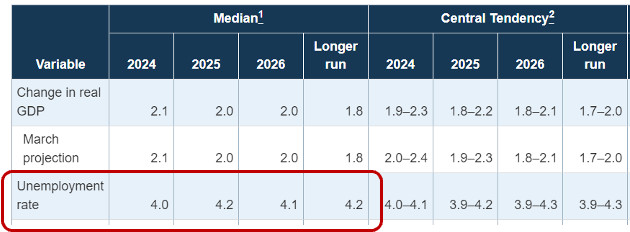

Using this latest figure on unemployment rate as a reference, the Fed's estimates are too conservative in our view. Table 1, highlighted in red, shows how significantly the U.S. central bank underestimates unemployment level. Over the next two years, the Fed expects the unemployment rate to remain around 4%, but we are already at 4.30%. Adding an additional 1.50% could push the rate close to 6%. If that occurs, GDP growth will almost certainly be affected.

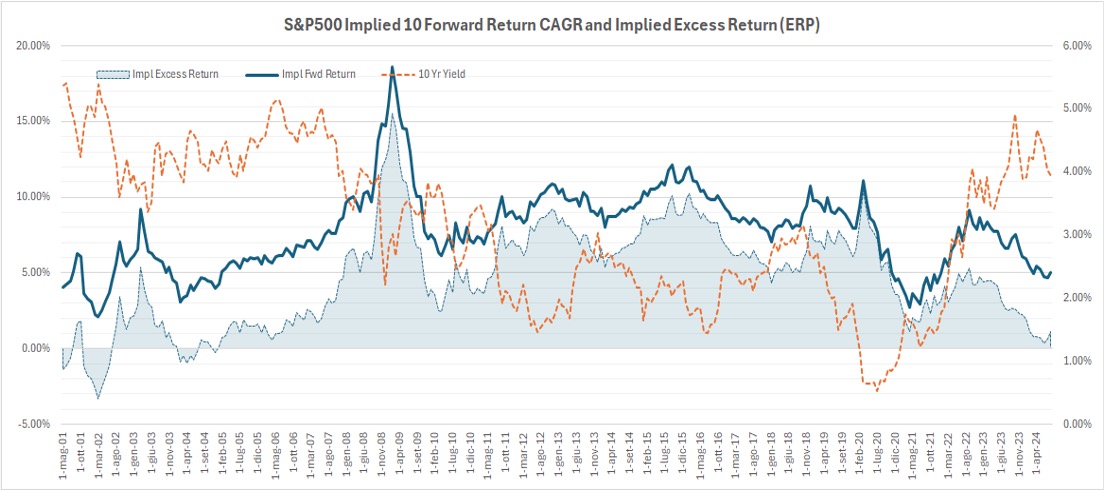

Based on our analysis, we continue to believe that a cautious approach to risky assets is appropriate and that it is better to favour investment grade corporate bonds. To support this view, we present a chart generated by our model, previously shared in past newsletters, which estimates the expected annual return on the S&P 500 over the next ten years (Chart 7). The Equity Risk Premium, or the excess return on equity investors will get from investing in equities relative to Government Bonds, is currently at 1.11%, remaining below 2021 levels, this same premium is available in investment grade bonds at no extra volatility cost. In our opinion, bonds continue to be more attractive than stocks, especially in light of the recent high volatility in the stock market.

About the author

LFG+ZEST SA