In the recent period the market seems to be very confused. The subsequent pairs of charts show that the dichotomy in the macroeconomic data is in stark contrast to the scenario currently discounted by the US equity market.

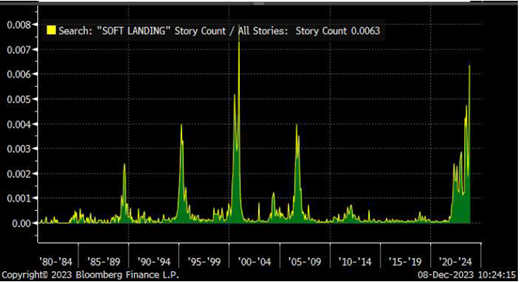

Chart 1 delineates the ratio of articles, stories and publications discussing about a 'soft landing' in relation to the overall total. Notably, this figure has surged recently, suggesting that investors are actively seeking confirmation for the potential occurrence of this scenario. This phenomenon can be called “Reflexitivity”, i.e. that investors are shaping their decisions not on objective reality but rather on their subjective perception of reality.

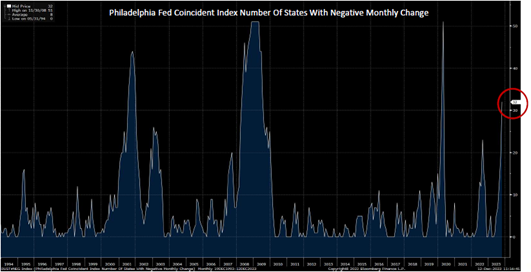

Conversely, Chart 2 presents conflicting signals regarding the likelihood of a soft landing. The count of U.S. states experiencing a deterioration in Coincident Indicators from the preceding month reached 32. Historically, a threshold indicating the probable onset of a recession is set at 20 out of the total 50 states.

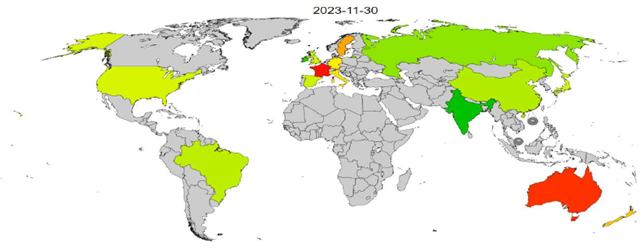

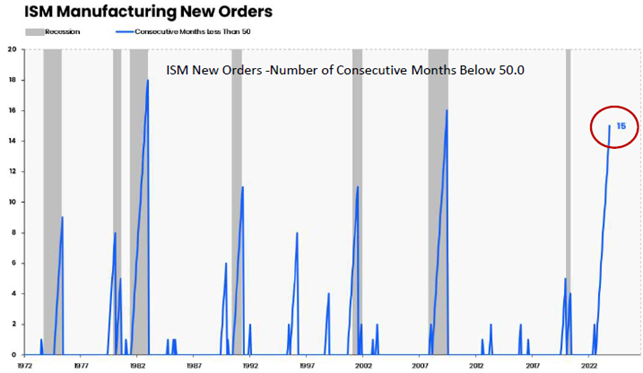

Below are two more representations of this discordance.

Chart 3 shows the Global services PMI; the green colour, although not intense, indicates that the last reading of the indicators was above 50, the threshold that divides economic growth from decline for a given country. Only France and Australia are in contraction territory.

Chart 4, on the other hand, represents the state of the manufacturing sector, specifically the number of consecutive months the index has been negative. The sector continues its prolonged decline.

Once again, the dichotomy between positive and negative aspects is underscored.

MARKETS DISCOUNTING A SOFT LANDING OR NO LANDING

Let us now shift our focus to interest rates and the valuation of the S&P 500 index to understand what the market is currently anticipating.

Concerning interest rates, the chart below illustrates the 1-year forward rate compared to the current 1-year rate. The market discounts that in one year’s time, interest rates will be about 90bps lower.

For such a scenario to unfold, it necessitates the continuation of falling inflation and the much-awaited Central Bank’s interest rate cuts. This will loosen the grip of restrictive monetary policy on the economy. As Chart 6 shows, real rates are currently at a very high level compared to the historical average and the longer they remain at these levels the greater the impact on the balance sheet of households and businesses.

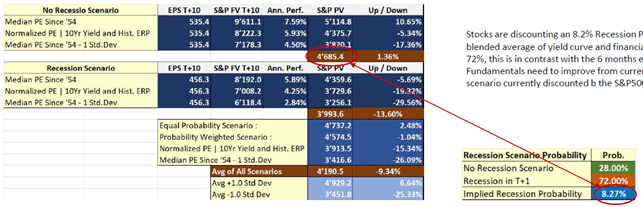

Looking at the stock market, Table 1 represents the outcome of the valuation analysis of the S&P500 index. As of today, the market indicates a probability of a recession at approximately 8%. Contrary to the data, the current index level suggests anything but a recession.

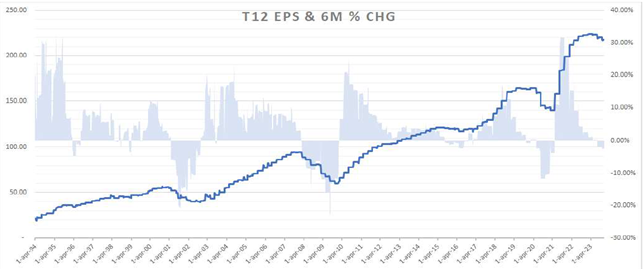

Returning to the initial argument, a stark misalignment persists between market assessment and financial and macroeconomic data. The chart below shows a clear example. The “Earnings Revision” of companies within the S&P500 index has been negative over the past three months. To rationalize the current valuations of the S&P500, the fundamentals of these companies would need to improve rather than deteriorate. As time goes by, if the situation remains unaltered, a substantial valuation issue is likely to emerge in the forthcoming period.

IF THE MAGNIFICENT 7 WERE A COMPANY

We recently conducted an analysis examining the performance of a huge company, consisting of 'The Magnificent 7' (Alphabet, Apple, Meta, Microsoft, Amazon, Nvidia and Tesla). We have consolidated the balance sheets of these companies to undertake a study that shows how these giants stand out from other entities. The key attributes defining this new 'invincible' company include robust growth, substantial cash flow generation, and financial stability.

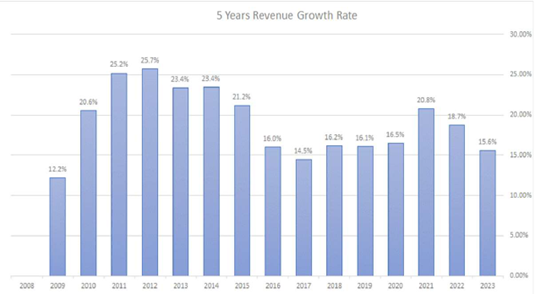

Chart 8 illustrates the 5-year average revenue growth rate, initially exceeding 20% and subsequently stabilizing at around 15%-16%.

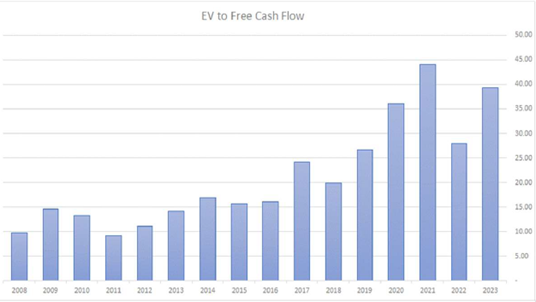

Thanks to these characteristics, the company's valuation has risen significantly over time. Chart 9 shows the EV/FCF ratio. This year, the share price rebounded significantly from the 2022 drop, almost reaching the 2021 highs.

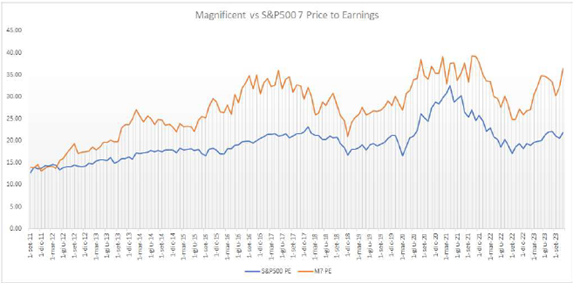

To understand even better how the market perceives the quality of these companies, Chart 10 shows the Premium P/E of the Magnificent 7 (orange line) compared to the P/E of the other companies in the S&P500 (blue line). In 2023, the P/E of the Magnificent 7 increased substantially, returning close to the levels of 2021. The huge difference between 2021 and 2023 are rates: in 2021 they were close to 0%, while in 2023, after the FED’s rate hikes, they are around 5%. Interest rates influence stock markets because they are used to determine the future valuation of a company. Lower interest rates are positive for stock markets, while higher interest rates reduce the future value of a company, so the valuation of equity market. Despite higher rates, the valuation of the Magnificent 7 are back to close to their all-time highs.

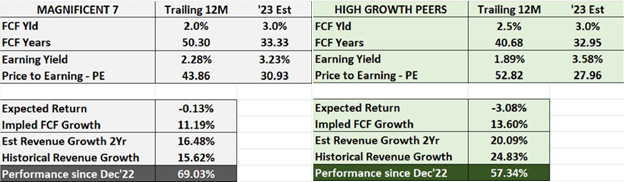

Continuing our analysis, we wanted to compare the Magnificent 7 with a basket of stocks that includes only companies that have achieved excellent YTD performance. These are all high-growth companies with at least 5 billion market cap and historical growth above 15%. We observed several similarities, as highlighted in Table 2, presenting a comparison of various metrics for these two baskets. The market performance since December 2022 is very similar, +69.03% vs +57.34%, as are the valuations in terms of FCF Yield, 2.0% vs 2.5%. The only difference concerns the Free Cash Flow Conversion, which is lower for the second group despite the latter growing faster given their smaller size. Additionally, a noteworthy observation pertains to the Expected Return. For the Magnificent 7, it stands at -0.13%, while for the other group, it is -3.08%. This figure implies that both groups are currently fairly values, with limited upside possibilities. However, in the event of a deterioration in the macroeconomic environment, the Magnificent 7, given their robust characteristics of high growth, high cash flow generation, and financial stability, may once again prove more resilient and better equipped to weather market downturns.

About the author

LFG+ZEST SA