“Prediction is the art of saying what will happen and then explaining why it didn’t.” – Karl Popper, philosopher economist, and statistician.

At the turn of the year, one of the most frequently asked questions, alongside what our good resolutions are for the upcoming months (which by the way we tend to forget by mid of January…), refers to our expectations for the economy and financial markets. This tendency is driven by the fact that all financial returns reset by the 1st of January. Yet, the economy does not.

This is why we try to distance ourselves from questions regarding “our expectations for 2024”, and rather focus on the bigger picture, overlooking the calendar. Instead, we try to answer questions such as what happened? Where do we stand? Where are we heading to? The first question is easy to answer. The second seems easy as well, but it does hide a few traps. However, it is the last question that inherently carries the greatest amount of risk in running into severe gaffes. Nevertheless, because we adopt a top-down approach in asset allocation, our starting point is based on what we expect from the future, at the risk of having to explain at a later stage why what we had initially forecasted never came true.

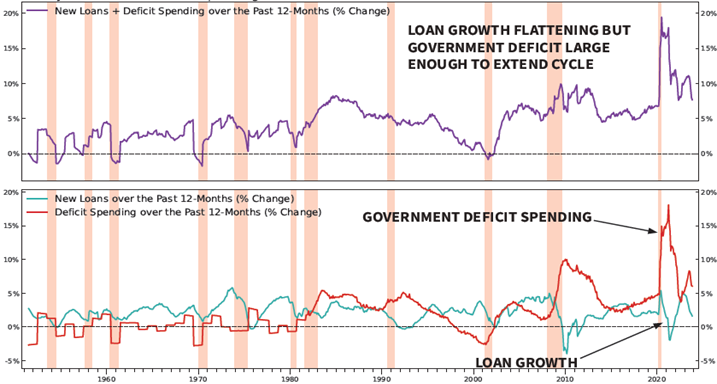

What happened? Despite interest rates being at a 20-year high (and the associated uncomfortable feeling towards the American commercial real estate sector), the second largest economy (China) being troubled by a real estate bubble, its main trading partner – Europe – flirting with a recession, and armed conflicts continuing and/or erupting anew, 2023 will be remembered as the year when the most expected recession in history never materialized, a clear example of reflexivity at play. We have recently written extensively about how the U.S. economy has been able to avoid the recession, thus we will not spend more time on this matter. Suffice to say that the strength of the U.S. consumer and the Federal government spending substituting banks’ loan growth have been the game changer.

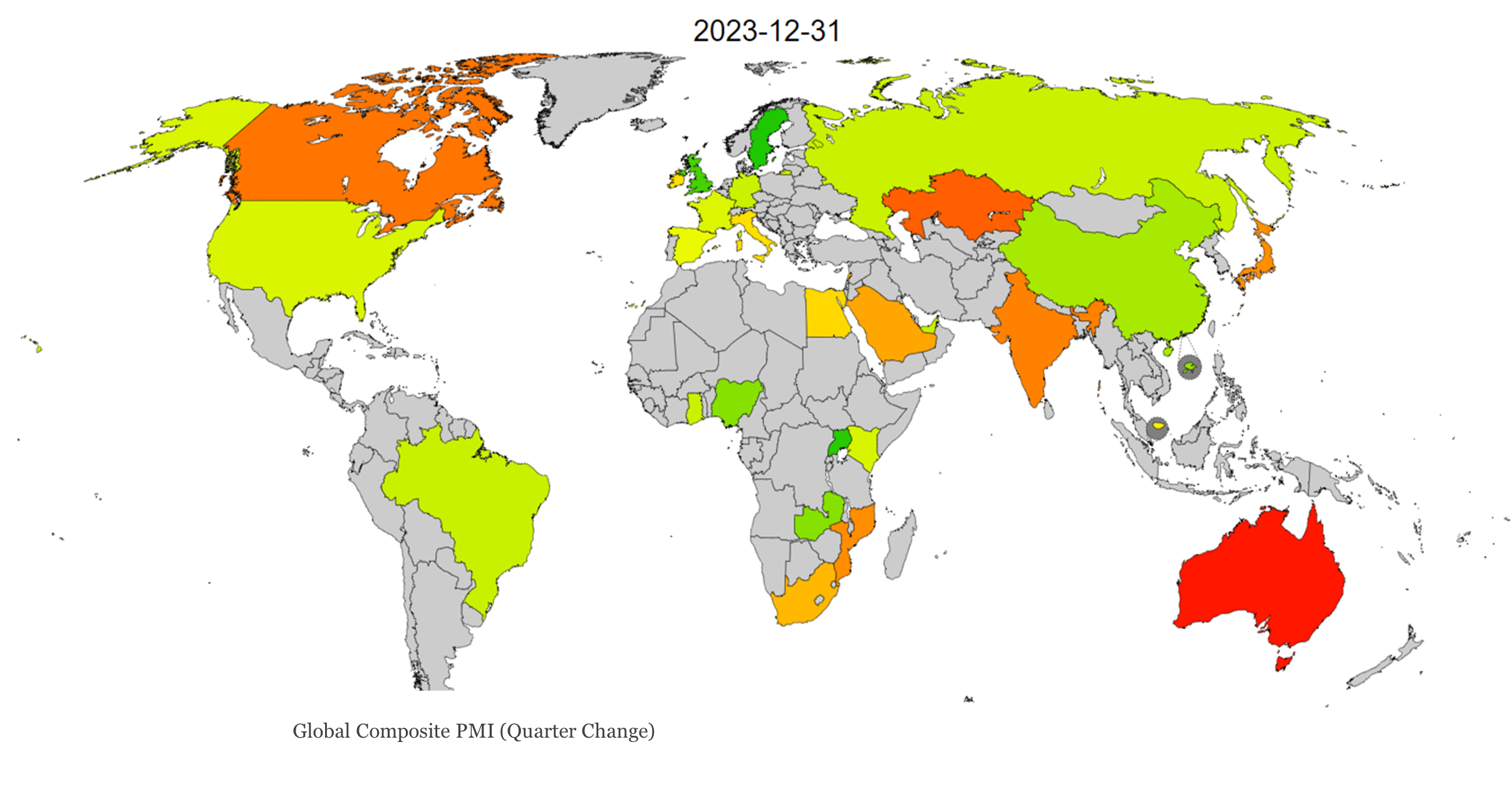

Where do we stand? As of this writing, the economic situation looks to be improving globally. The soft-landing narrative has gathered pace, fuelled by forward-looking surveys (the Purchasing Manager Index – PMI – to mention one) that show an improvement compared to the previous quarter (chart top-right), along with the inflationary pressure that is slowly abating, and the labour market that continues to show signs of normalization.

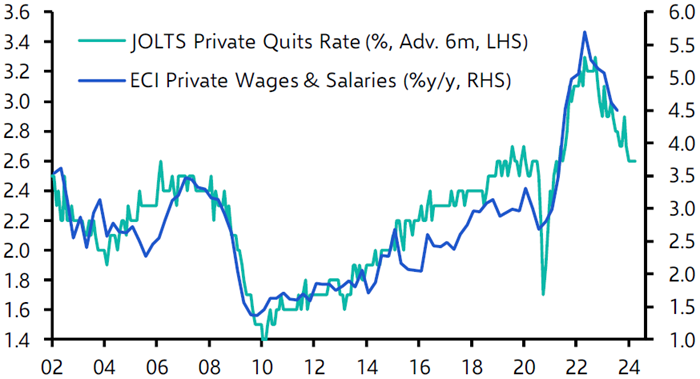

More specifically, while core inflation has recently stabilized close to 4%, a level that is still twice the central bank’s target, it should be only a matter of time before the deflationary pressure from lower housing rents kicks in. A similar picture can be observed when focusing on wage growth (chart to the left), an important element in determining the inflation rate; the current level still hovers around 4.5%, roughly 1% above what the Federal Reserve (FED) considers to be consistent with an inflation rate of 2%. However, the normalization currently underway (the job quit rate is back to pre-pandemic levels) bodes well for wage growth to fall further.

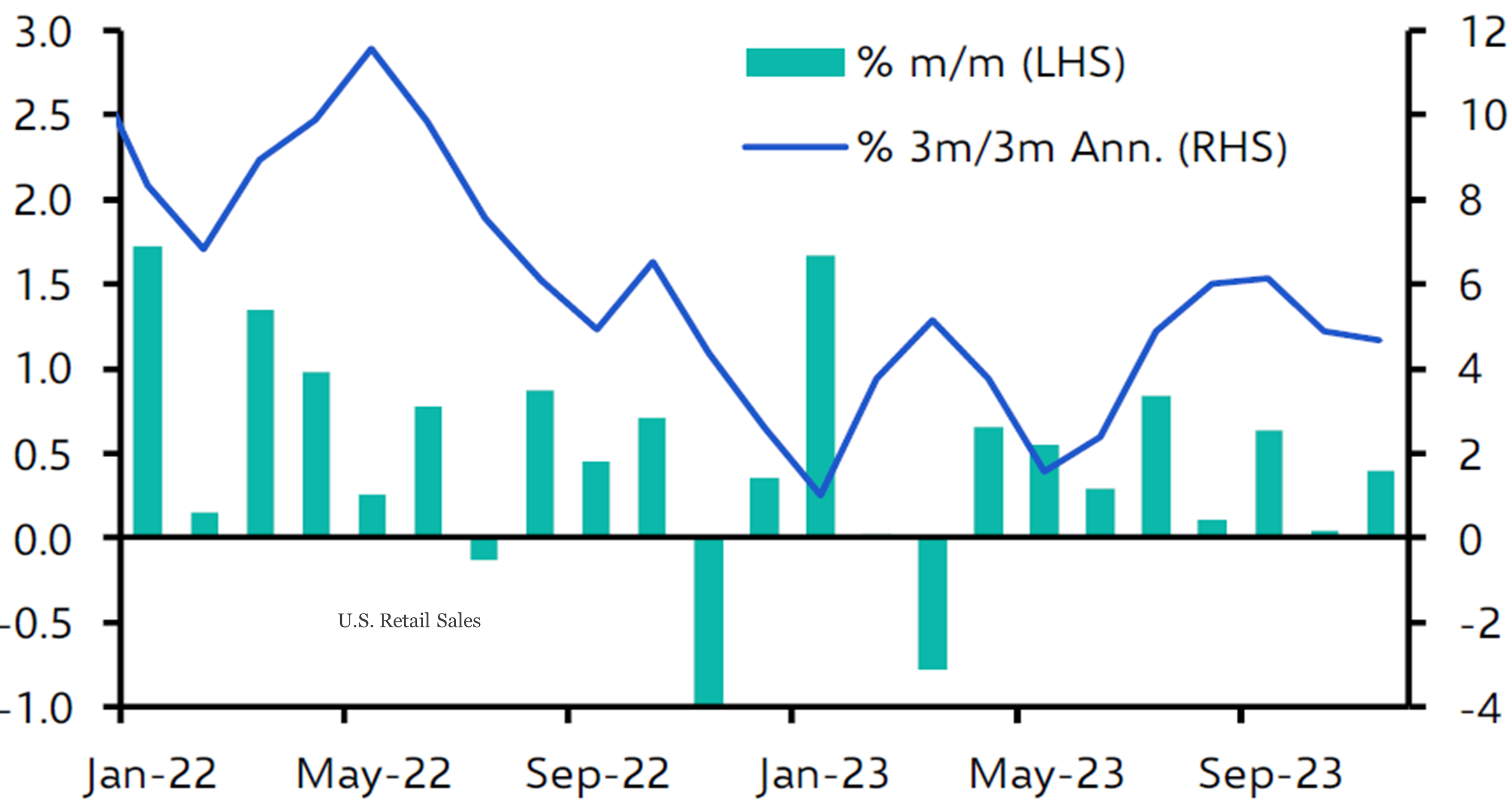

Admittedly, we can understand why half of the economists out there, and judging from the financial markets returns of the last couple of months, the vast majority of investors, believe that a soft-landing is in the making. As noted, the economy seems to be normalizing without falling off a cliff, while household consumption remains resilient (chart to the right) and 2008-like excesses are no where to be present. In fact, the balance sheet of American families seems stronger than ever, despite terrible financial returns in 2022 and housing affordability close to all-time lows. But interestingly enough, the latter has only marginally affected the housing market, usually one of the sectors to succumb the earliest in anticipation of an upcoming recession. The private deleveraging post Great Financial Crisis, supported by more stringent bank credit standards, has ensured a lower supply of homes, which is compensating what we believe to be a natural decline in the demand for houses. Dulcis in fundo, according to many, both on Wall Street and Main Street, the FED is ready to embark on a massive round of interest rate cuts (six for 2024), granting the necessary support to the economy to avoid decelerating excessively, thus avoiding a recession. Makes sense.

Where are we heading? At the risk of becoming the latest proof in support of Mr. Popper’s statement, we take a look into the future, trying to envisage (avoiding the use of the word forecast is deliberate, we don’t want to make it too easy for Mr. Popper to be right) the potential risks around the consensus for a soft-landing.

Let’s be clear; soft landings are extremely hard to achieve. The reason being that authorities act on published data that is backward looking, i.e. that represents the past (GDP, unemployment, inflation rate, etc.), making the former chronically late in their decision-making, not for a fault of their own, but simply because the economy evolves on a daily basis. Also worth noting is that an economy always transitions through a soft-landing state before it enters a recession; GDP growth rarely falls from high-single digits to negative figures. The deterioration takes time, and GDP growth first abates, and then falls into negative territory. It is the phase characterized by the abating that sparks hope for a soft-landing.

If we look at the past instances of soft-landings (only three), these have never happened with an inverted yield-curve. Why is the inversion an omen for an upcoming recession? No magic involved, but a rather simple explanation; banks borrow short-term, and lend long-term. When the curve is inverted, the business becomes less profitable (short-term borrowing is more expensive than long-term revenues), and banks are less incentivised to issue credit to businesses and households, removing an important source of growth. Today, the curve is inverted, and has been in this state for almost two years. A long time.

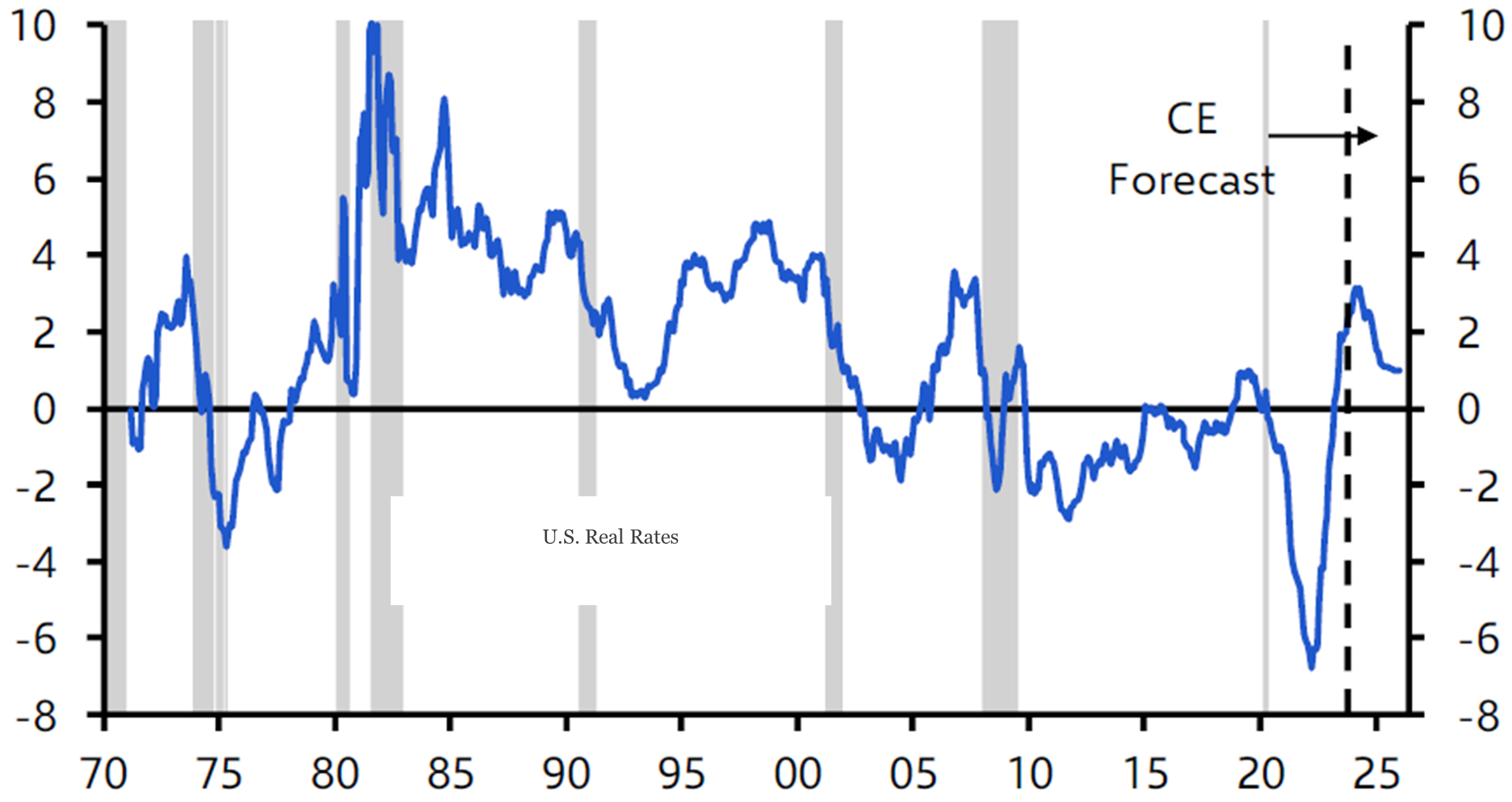

A lot of the exuberance witnessed in financial markets can be traced back to the expectations of meaningful rate cuts to be delivered during 2024. On this topic, as we have already outlined in the past, we remain sceptical. With a resilient consumer base, core inflation at 4%, and a labour market that is far from possibly being defined as weak, cutting rates could have the adverse effect of setting off another wave of inflationary pressure. On the other hand, with real rates (real rates are nominal interest rates less inflation, and represent the effective interest rate the economy is exposed to – chart to the left) back in positive territory, the economy is exposed to tighter financial conditions, and the FED is eager to cut rates to engineer the abating phase mentioned earlier. But it cannot do so unless the economy deteriorates further, risking a recession. For the moment, it seems stuck between Scylla and Charybdis 1.

The yield curve inversion has caused bank lending to contract. So how come the economy fared well, nevertheless? Fiscal support, first directly to households in the form of helicopter money, and later in the form of incentives to businesses and infrastructure spending, has more than compensated the vacuum left by banks (chart to the right). Can this last? The U.S. government is currently running one of the widest deficit of the post-World War II era, without being in a recession. In theory, there are no limits to how large the deficit can grow, and 2024 is an election year, thus we doubt the Biden administration will reign in on spending. But we find it hard to believe it can grow much further. With household excess savings trending towards zero, the risk that the economy begins hiccupping is not irrelevant.

A year ago, we were convinced the U.S. economy was ready to fall into a mild recession. Twelve months later, we are explaining why it didn’t. Still, the possibility that our view has been delayed rather than proven wrong is real and we believe the next couple of quarters will be very important in determining the economic path we are embarking on.

Moving on from the United States, the economies of both Europe and China continue to struggle. Germany, the engine of Europe, is faltering. Industrial production has been on a declining path since the onset of the pandemic, with tight monetary conditions, rising energy costs, and a slowdown in China, Europe’s main trading partner, not helping, to use a euphemism. The decline in the German output has been partially compensated by the strong results of services-oriented countries such as Italy, Spain, and Portugal, which have benefited from a wave of spending following the pandemic lockdowns. The recent rise in interest rates have hit Europeans the hardest because they are more exposed to floating-rate debt. However, the trillions amassed by consumers during the pandemic are largely spent in the US but continue to grow in Europe, despite an initial spending spree. Excess household savings currently amount to 14% of annual incomes, up from 11% two years ago, which may limit the magnitude of the economic slowdown we are experiencing.

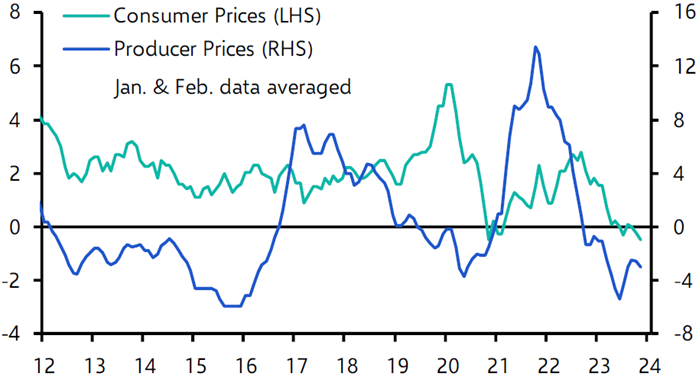

Chinese economic activity has improved moderately over the last few years, supported by low but relentless stimuli, aimed at stabilizing a battered economy, but mindful that a significant reacceleration in activity could be detrimental to an indebted nation. Slowing external demand for Chinese goods, coupled with the recovery of supply chains, has sent the Chinese economy in a deflationary state (chart to the left). While this is negative for internal productivity and growth, it is positive for the outside world, as China is de facto exporting deflation, helping developed economies in their battle against rising prices. We expect the Chinese economy to remain under pressure until the issues related to the real estate sector are finally cleared.

FIXED INCOME: MORE OF THE SAME

2023 has been a volatile year for fixed income investors. In fact, during the last couple of years, volatility in fixed income prices has remained elevated, and much above the long-term average. The massive repricing witnessed in the months leading up to 2024 only represented the latest proof. With the U-turn of the FED, US government rates fell by roughly 100 basis points across the yield curve. This means, 10Y government bonds returned an outstanding 9.5% over November and December. A similar destiny has been reserved for both investment grade bonds and high yield bonds which, over the same period, have offered similar returns.

Indisputably, the expectation of a looser monetary policy has propelled prices. Similar to equity prices, as we shall see shortly, investors are currently pricing a risk-free world; at these valuations, markets are telling us that there are literally no chances monetary authorities will commit some sort of policy mistake, nor is there any chance that the soft-landing turns out to be a turbulent-landing. We would avoid painting everything with the same brush.

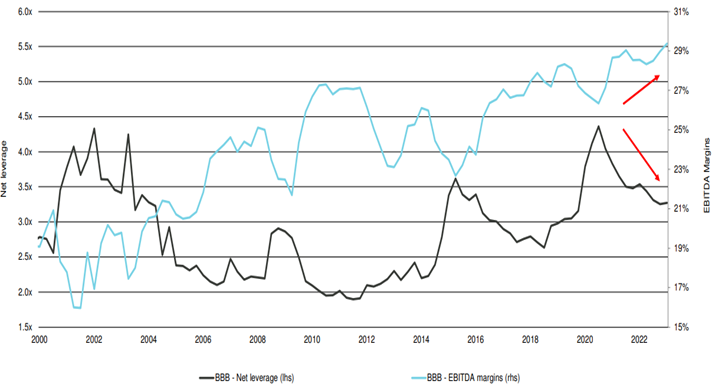

If we look at fundamentals, we rest confident in the ability of investment grade companies to withstand a slowing economy, as net leverage has been declining and is close to the 20Y-average, while EBITDA margins remain on a long-term rising trend (chart to the right). Therefore, it is no surprise that the quality of the investment grade sector is strong and continues to improve, as the share of BBB-rated companies has been falling in favour of higher-rated issuers since the peak was reached at the end of 2021. Valuations are not cheap, but they are not expensive either, making the sector a compelling investment, especially with the retracement of interest rates witnessed during the first trading weeks of the new year.

The U.S. government is currently running one of the widest deficit of the post-World War II era, without being in a recession.

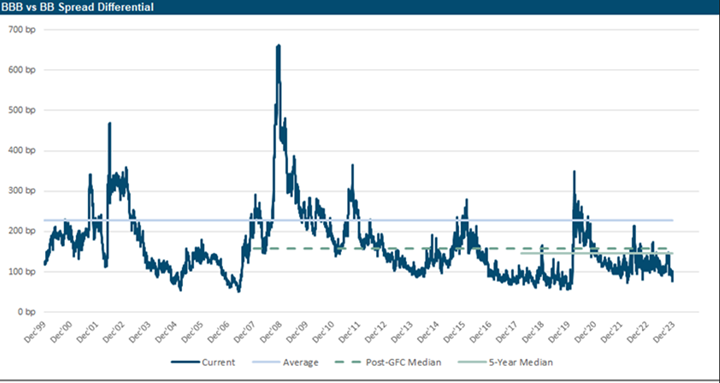

On the contrary, the high yield segment of the market does not seem to be pricing the possible effects of a downturn in the economy. Default rates have been on the rise over the past few years, both in the U.S.A. and in Europe, but over the same period, the returns of the segment have been by far the best ones within the asset class. Something does not add up. The rating drift also speaks in favour of the investment grade companies, as the number of high yield upgrades lags the number of downgrades (it is the opposite when looking at investment grade issuers). With fundamentals deteriorating, noting that both relative and absolute valuations are rather expensive (chart below) and above the long-term average makes us turn our nose up. An opposite situation compared to emerging markets issuers, whose fundamentals appear in good shape, especially if what lies ahead of us is a period characterised by a weakening U.S. dollar, and whose valuations are rather interesting (more on the currency front rather than credit spreads).

One last remark on the overall level of interest rates; at the beginning of the year, many investment professionals we talked to were expecting 2024 to be the year of bonds, a similar thinking we bumped into during the beginning of 2023 (friendly reminder: while the view turned out to be correct, as of the 31st of October, bond returns excluding high yield issuers were in the red, and only later saved by the FED). We can assume interest rates will fall should the economy begin to contract – and this means the effect on corporate bonds will be mixed, depending on the quality of the issuer – but we continue to adopt a cautious approach with respect to the inflation trajectory; in a nutshell, we are not as confident as the market is that inflation will fall back to the FED 2% target as soon as this summer, and thus we leave the door open for interest rates to remain elevated over the course of 2024, creating further volatility investors will be obliged to manage.

EQUITY: CONCENTRATION NOW MATERIALLY RELEVANT

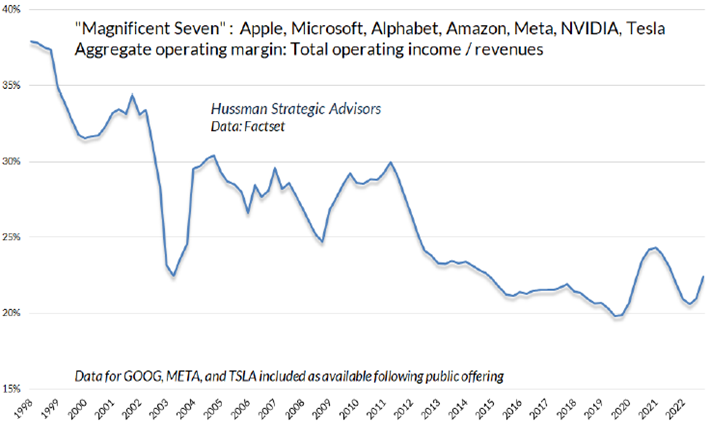

If we were to focus solely on the future, we would unveil several encouraging premises for equity prices to continue their year-long bull market. In 2024, supported by the assumption that we are going to witness a soft-landing scenario, consensus expects earnings to grow on average by roughly 10%, following two years of sluggish growth. Moreover, as companies have kept their forward guidance on the safe side, the probability of beating expectations is high (Q4 earnings are being published as we write, and with 10% of the companies having reported, the earnings surprise is in the high single-digit camp). The expansion of margins should contribute meaningfully to the rise in earnings, as the former have also begun to recover following the trough reached mid of 2023 and are expected to continue growing for the year.

The soft-landing scenario is still being debated among economists, who are evenly split between believing and disbelieving. Yet, the semiconductor industry, a leading indicator for the world’s economy, is showing tentative signs of rebounding – as we write, Taiwan Semiconductor reported strong results, with the share price jumping 9%; both chips’ sales and prices have started to recover. A further boost to the economy could also come from artificial intelligence (AI); the narrative surrounding AI gave a boost to stock prices in 2023; the actual implementation of AI in the production processes may provide a boost in companies’ earnings in 2024, and beyond. Moreover, this is an election year which, judging by past standards, has often generated positive returns for equity investors. And while the valuation of the S&P 500 is expensive, the valuation becomes less expensive if we focus our attention on the S&P 500 equal-weight index (this is because the bigger companies – i.e. the Magnificent 7 – which are also some of the most expensive ones, carry a much smaller weight in the equally-weighted index). Thus, if we were to focus solely on the future, we have reasons to be optimistic. But…

…if you are a habitué of our publications, you should know by now that we always show there are two sides to the same coin. Looking solely at the future is like driving a car without ever looking at the rear-view mirror; risks can come from the past, as much as this may sound counterintuitive.

The primary risk we face is that equity markets are priced for perfection. What this means is that they don’t allow room for errors nor the (many) uncertainties we face going forward. The result is that, should the idea of a soft-landing vanish, or should interest rates begin to rise again due to a resurface of inflationary pressures, equity markets will have to adjust accordingly. Related to this is the fact that earnings expectations seem somewhat too rosy – again, no risks are priced in. But a year ago, analysts expected 2023 earnings to rise 10%, and the reality turned out to be much different. They have now shifted their growth expectations to 2024 (much as we did with our recessionary view…), on the assumption that the economic recovery will propel the bottom line of businesses. And while it is certainly true that election years very rarely coincide with economic downturns and/or poor equity returns, we must highlight that 2023 was an incredibly strong year for equity markets, thus some of the action that was supposed to be taking place in 2024 may have already taken place.

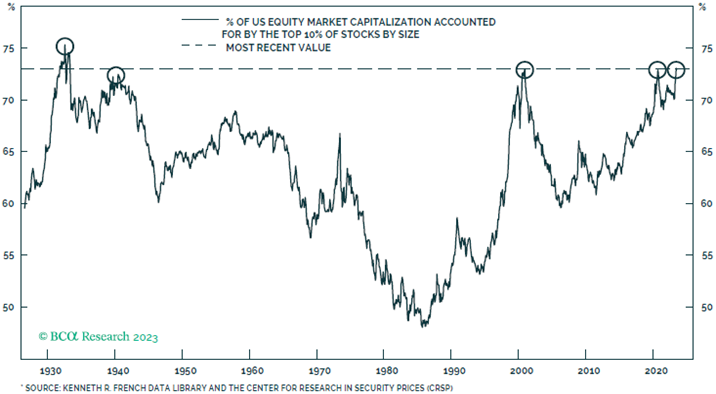

Market concentration is also a factor that should not be overlooked (chart top right). Currently, the Magnificent 7 account for over 30% of the total market value of the S&P 500, the highest in history. When market concentration has reached such levels in the past, the following years have always been characterized by volatility, to say the least. Furthermore, the concentration focuses on companies – the Magnificent 7 – whose growth rate is set to decelerate as they take on a bigger share of the pie. More generally, it is important to remember that companies’ earnings cannot grow at elevated rates in perpetuity. And the Magnificent 7 will be no exception.

Lastly, as we always point out, valuations remain expensive. 2023 saw no meaningful earnings growth, while the stock market returned roughly 25%, which is to be attributed entirely to multiple expansion. As a result, valuations are higher today than they were a year ago, and back then they were not cheap. We always say that valuations are not a reason for markets to fall but they impact the expected returns given a dollar of investment; the higher they are today, the higher the returns you have (possibly) made in the past, the lower the returns you should expect in the future. Valuations are your rear-view mirror.

CURRENCIES AND COMMODITIES: GEOPOLITICS REIGNING IN

Addressing commodities is akin to discussing emerging markets; attempting a broad approach seems increasingly nonsensical. Commodities are at times highly uncorrelated with each other; hence we must differentiate between energy (often politicized), industrial metals (linked to global growth and specifically to the Chinese economy, the main customer), and precious metals (a safe-haven asset and inversely correlated to real interest rates). The current environment requires prudence when managing cyclical commodities such as industrial metals; as we noted earlier, the Chinese have not yet emerged from the muddy waters they have fallen into a few years ago. Energy, on the other hand, has many supporting factors, ranging from geopolitical risks arising from the conflict in the Middle East, to a pick-up in demand from specific emerging markets economies. Moreover, taking a longer-term view, we are sceptical that the energy transition will occur as fast as authorities hope for, which means we shouldn’t make the mistake of dismissing the black gold so fast. Finally, gold has done incredibly well in 2023; a rising demand by global central banks and renewed geopolitical risks more than compensated skyrocketing real rates. Looking forward, we expect the first two factors to persist, while we envisage real rates to change their trajectory, increasing the list of supportive elements for the yellow metal.

What could hinder a renewed bounce in the price of gold is a stronger US dollar. The path of the greenback continues to be interest rate-driven; if the FED does embark on an interest-rate cutting spree, the USD is bound to weaken further. Only a renewed tightening of financial conditions, and related financial stress, could make the USD appreciate. Over the long-term however, valuations don’t play in favour of the USD. Overseas, we expect the EUR to move in a big trading range against the USD, given it is facing similar challenges as well as prospects as the United States. A stronger balance of payments will most likely be compensated by a weaker economy. In Switzerland, the Swiss National Bank has continued to purchase Swiss Francs to unload foreign currency reserves. It is expected this amount should start to be reduced, and together with looming rate cuts, the CHF should start to slightly depreciate against its major peers2.

About the author

LFG+ZEST SA