“What is right is not always popular, and what is popular is not always right.” – Albert Einstein, Physicist

ECONOMY: UNNECESSARY STIMULI

The Great Financial Crisis (GFC) of 2008 shaped an entire generation of investors and policymakers. No, don’t worry – I am not about to draw direct comparisons between today’s environment and back then, nor to search for similarities that might justify an overly cautious stance in light of my (alleged) bearishness. My intention is simply to highlight that the GFC marked a turning point in the implementation of monetary policy.

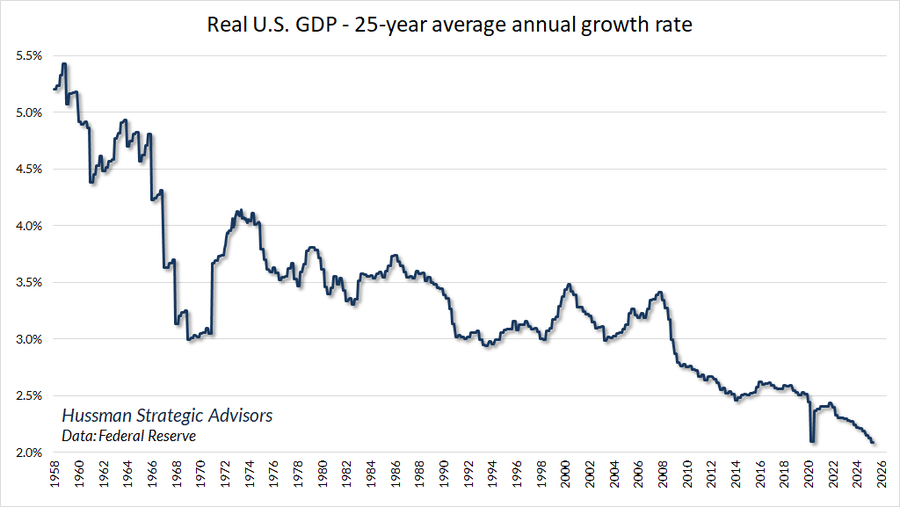

To put it bluntly, the amount of liquidity injected into the system since then has been almost pathological – certainly far beyond what would have been necessary to sustain a 2% inflation rate. In the name of GDP growth, interest rates were kept extremely low and, as the pandemic struck, pushed to the zero bound. With both quantitative and monetary easing in full force, one might have expected real GDP growth to soar. It did not. Economic growth ultimately depends on demographics and productivity – both of which have remained sluggish for the past two decades.

A decade of ultra-low interest rates has failed to generate meaningful growth (to put it mildly), and the fact that 5% rates have only lightly affected the economy suggests that GDP growth is now less sensitive to monetary conditions. Moreover, cutting rates when the economy is running above potential (positive output gap), and with inflation still well above the 2% target, may endanger price stability. What’s more, as reflected in the latest dot plots, FOMC members have raised their forecasts for GDP growth and inflation while also projecting lower unemployment for 2026. Is this really the right backdrop for pro-cyclical policy moves? The question seems legitimate.

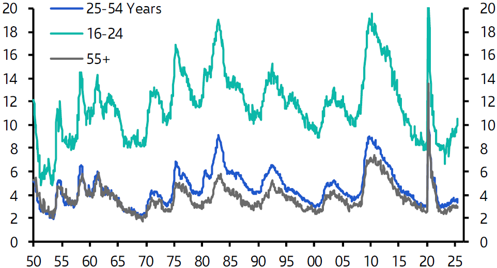

To be fair, the job market has been gradually softening over the past couple of years, and the revisions published this summer painted a somewhat grimmer picture than initially reported. Youth employment (age 16–24) is a particular area of concern; uncertainty over tariffs and the rise of artificial intelligence appear to be making firms cautious about hiring. Still, the deterioration in labor data does not point to a recessionary trend – rather, to a prolonged normalization. This interpretation is supported by resilience and even improvement across other areas of the economy.

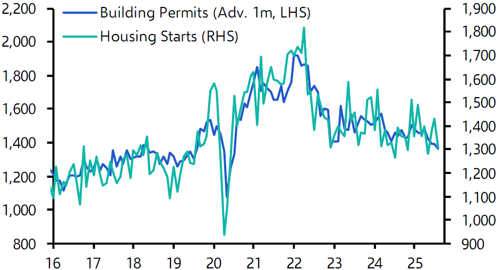

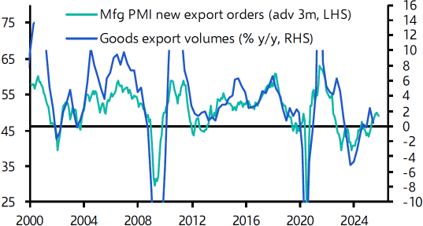

Manufacturing indicators, for instance, have begun to rebound. After nearly two years in recessionary territory, the end of the tunnel may finally be in sight. The 30-year mortgage rate has fallen by over 150 basis points, stimulating demand and enabling homebuilders to offer lower rates to buyers. Certain parts of the housing market, particularly commercial real estate, remain under pressure as new habits (remote work, the gig economy, etc.) become entrenched. Yet the broader housing market never suffered major setbacks, as a persistent undersupply has offset subdued demand. The absence of sector-wide layoffs underscores that the housing market remains fundamentally balanced.

As we have consistently argued, households are in good shape. Little has changed since our summer assessment. Strong financial market returns have supported consumption through the wealth effect, household balance sheets remain largely unlevered, and the savings rate is low – all of which bode well for ongoing economic expansion. Real consumption spending continues to grow solidly and may well remain robust through year-end, aided by falling rates.

Beneath the surface, however, the story is more nuanced. The top 10% of earners – who account for roughly 40% of total spending – are indeed thriving. But as we move down the income ladder, a significant portion of the population is struggling to meet basic needs, as reflected in rising default rates. While this inequality will eventually carry economic costs, the strong balance sheets of banks and credit card issuers should prevent any broader contagion.

All told, the U.S. economy remains in good shape. Admittedly, looming tariffs and tighter immigration policies are risks that cannot be ignored. Despite the administration’s much-touted trade agreements, the full economic effects of tariffs have yet to materialize – thanks to exceptions, postponements, transition periods, and firms temporarily absorbing higher costs.

Tighter immigration policies could have profound implications. U.S. corporations may be forced to replace foreign-born workers with domestic ones – easier said than done. Over the past five years, foreign-born workers accounted for the vast majority of job creation, especially in lower-paid roles. Will Americans be willing to fill these positions? Meanwhile, labor force growth is slowing, meaning that fewer new jobs are required to maintain a stable unemployment rate – around 150,000 today, falling to just 50,000 in the future. The breakeven rate, in other words, is declining.

Both tariffs and lower immigration share a common outcome: upward pressure on prices. Whether this proves temporary or persistent remains to be seen, but leading indicators already point to renewed inflationary trends – starting from a level well above the Fed’s 2% target. Lower immigration will likely push wage growth higher, not lower. Similarly, the full imposition of tariffs will at best keep prices steady – if one wishes to be optimistic.

In sum, we believe the U.S. economy does not require additional support. Yet the fiscal deficit is projected to rise, and the Federal Reserve is expected to cut rates five more times before the end of 2026. This dual stimulus raises the risk of overheating, potentially driving inflation well above target.

Turning to Europe, the picture resembles a modest Goldilocks scenario: mild growth, contained inflation, and stable unemployment allow the ECB to maintain a wait-and-see stance. Manufacturing is improving, buoyed by expectations that Germany’s fiscal stimulus will finally lift the eurozone core out of its lethargy. Private consumption remains tepid – most of the recovery stems from fiscal expansion rather than organic demand – but for once, let us appreciate the moment. The here and now, as Asian cultures practice. Despite internal political tensions and existential debates over Europe’s identity, the economic outlook remains favorable: tariffs discussions are off the table (for now), and the ECB still has ample ammunitions if needed.

China, by contrast, continues to battle a balance-sheet recession, worsened by trade disputes with the United States. Although the government has rolled out several consumption-support programs with decent initial results, these effects faded quickly, exposing the structural fragility of the economy. The real estate sector remains the primary drag. After a brief rebound following state-backed home purchases, the market has resumed its decline. A glut of unsold housing inventory continues to weigh on recovery efforts. More stimuli will be required—but even in Beijing, ideas seem to be running thin.

FIXED INCOME: THE INVESTABLE UNIVERSE IS SHRINKING

The path of interest rates has diverged markedly between the United States and Europe. The European Central Bank has cut its main refinancing rate several times this year, bringing it down to 2.15%. Combined with Germany’s fiscal expansion plan, this has led to a modest steepening of the European sovereign yield curve – suggesting expectations for stronger growth ahead.

Across the Atlantic, by contrast, the Federal Reserve has remained largely on hold (except for September’s cut), prompting a parallel downward shift of the U.S. yield curve. This could be interpreted in several ways, including that some bond investors expect growth to slow because the Fed is not easing policy quickly enough.

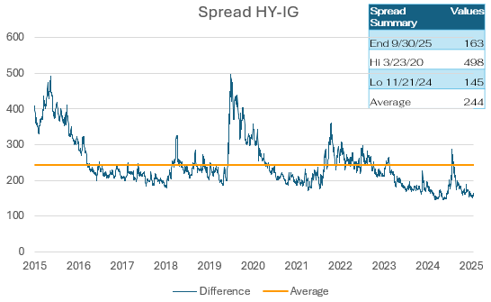

Be that as it may, our fixed-income stance remains largely unchanged. In a world where most asset classes appear expensive, investors should focus on securities offering the most attractive risk–return trade-offs. In our view, investment-grade corporate bonds continue to fit this description: fundamentals remain solid on both sides of the ocean, the rating drift favors upgrades over downgrades, and valuations look more compelling relative to high-yield or emerging-market debt.

As you may recall, over the past year we have been notably constructive on subordinated debt. The picture there remains broadly positive: both financial and corporate issuers maintain strong balance sheets, and profitability is at record levels. However, signs of froth are beginning to appear. Specifically, the overwhelming demand for yield, irrespective of risks, is compressing coupons and yields to maturity on primary issuances. As a result, valuations have become less attractive on a relative basis.

From a duration perspective, we continue to advocate a conservative stance; widening fiscal deficits, mounting debt burdens, and the return of a positive term premium all argue for keeping portfolios positioned toward the shorter end of the curve.

In this environment, valuations tend not to matter…until they suddenly do.

EQUITY: PRICE CORRECTIONS, SAY WHAT?

Earlier, we noted that the US economy remains robust, supported by a solid services sector and an emerging recovery in manufacturing. But will this translate into faster earnings growth? And if so, will that in turn feed through to higher equity prices?

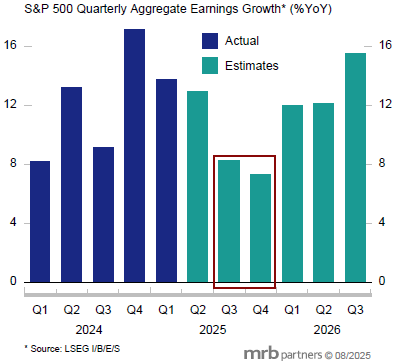

Let’s start with the data. In the second quarter, U.S. corporate earnings grew by nearly 13% year over year, with revenues up more than 6%. Positive earnings surprises in the communication services, technology, and financial sectors accounted for most of the upside; excluding them, earnings growth would have been a modest 2% Y/Y. For the second half of the year, consensus expects high single-digit EPS growth – slightly lower than in previous quarters, as the impact of tariffs begins to bite. Even so, EPS forecasts have been trending higher, supported by resilient results from technology, communication services, financials, and select industrials.

Overall, the market has reverted to a two-tier structure, with a handful of sectors and companies driving aggregate results. Earnings growth remains above trend, and operating profit margins are at historical highs.

However, consensus still assumes aggressive margin expansion ahead – an ambitious outlook given the starting point, tariff risks, the growing capital intensity of Big Tech, and the rising costs of reshoring. Even if U.S. growth accelerates further, we doubt that earnings will keep pace: likely gains among cyclical sectors could be offset by normalization among the top performers.

Stock prices, meanwhile, may continue to rise – unless something breaks structurally. In this environment, valuations tend not to matter…until they suddenly do. Traditional metrics already point to significant overvaluation, even after accounting for strong cash flow generation. Still, investors can take some comfort from the fact that corporate balance sheets are exceptionally healthy. Most companies refinanced debt when rates were near zero, so refinancing risks remain limited for at least another five years.

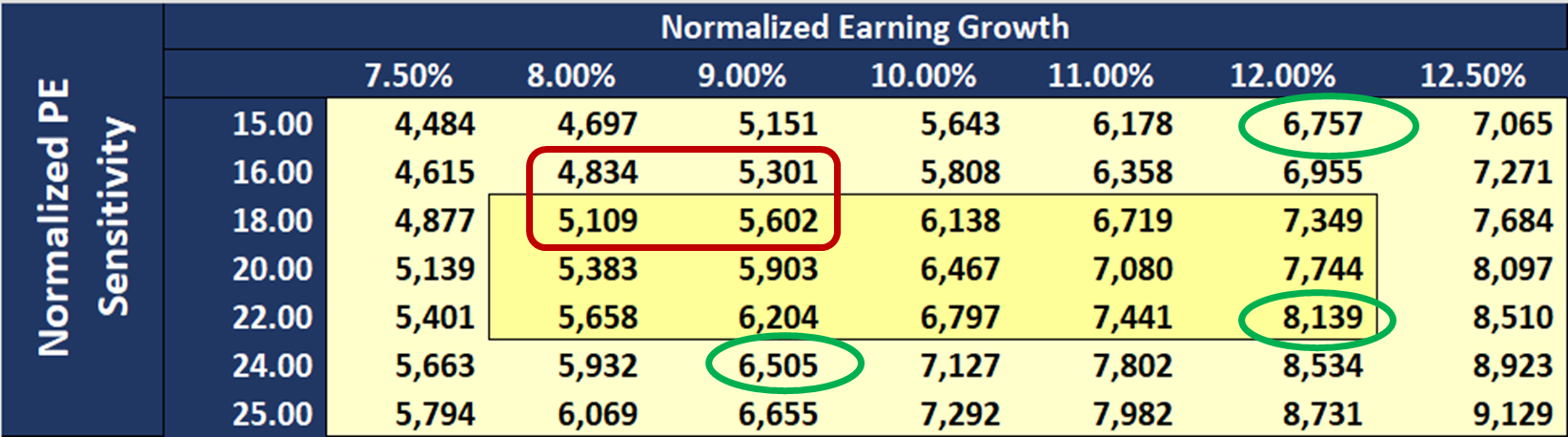

As shown in the table below, the current level of the S&P 500 effectively discounts one of two scenarios: either a normalization of the price/earnings ratio back to 15x while sustaining 12% earnings growth, or a slowdown in earnings growth to 9% while maintaining a 22x P/E multiple. It does not discount a recession (which we also deem unlikely), but neither does it reflect a normalization in both earnings and valuations, an outcome that would imply an index level near 5,000, or a continuation of both at elevated levels (around 8,000).

In short, the S&P 500 remains priced for perfection – meaning investors should be prepared for bouts of heightened volatility whenever the narrative wavers.

From a sectoral perspective, healthcare stands out as an obvious value play: companies in this sector generate robust free cash flow and currently trade at attractive valuations. “As goes tech, so goes the market” still holds true, so maintaining exposure to technology remains essential, at least in relative terms. Financials should also benefit from a gradually steepening yield curve.

Conversely, energy, consumer staples, and consumer discretionary sectors could face headwinds: energy from rising supply, staples from softer consumption among lower-income households, and discretionary from the looming effects of tariffs.

In Europe, equity market performance has been lackluster since early March. The Stoxx 600 has gone essentially nowhere. This underperformance relative to U.S. equities likely reflects the newly imposed U.S. tariffs, as well as euro appreciation, which further undermines the competitiveness of European exporters. A limited technology sector and a chronic innovation gap complete the picture.

There is, however, some good news. Europe’s private-sector deleveraging phase is largely behind: leverage is down, liquidity is ample, and debt-service metrics are healthy (with France as a notable outlier). Repaired bank balance sheets and improving profitability position Europe’s bank-centric financial system to better finance growth and capex.

Moreover, Europe is pivoting away from a decade of austerity toward moderately expansionary fiscal policy – led by Germany. This shift could help unlock new momentum for corporate earnings.

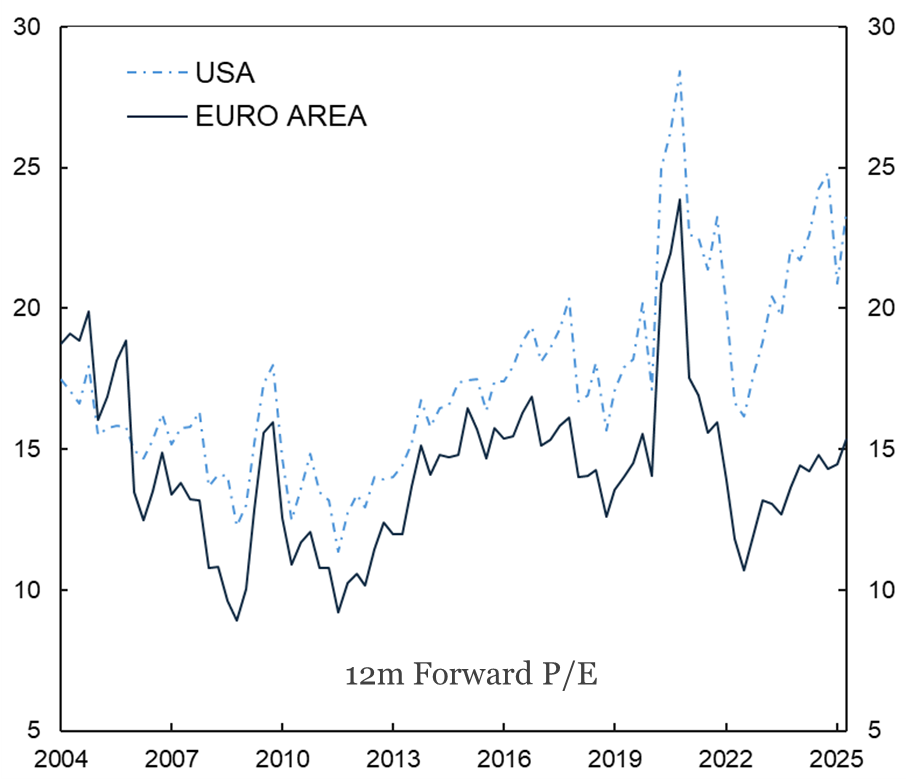

Valuations also provide room for multiple expansion: European equities still trade at a significant forward P/E discount to the U.S., and the gap is broad-based across sectors. In today’s market, that relative cheapness offers a cushion against downside risk, contrasting sharply with the AI-driven concentration seen in the U.S. However, we do not yet believe it is time to fully rotate from U.S. equities into European ones.

CURRENCIES AND COMMODITIES: LITTLE HOPE FOR THE USD

The fate of the U.S. dollar remains one of investors’ main preoccupations – ours included. Fundamentally, the dollar remains overvalued, even after this year’s sharp decline. Yet, as in all markets, valuations matter only over the long term. In the near term, currency moves are driven by interest-rate differentials, geopolitical developments, and technical positioning. The first two are inherently unpredictable; the third currently favors the greenback, as positioning has become excessively bearish.

The key uncertainty lies in rate expectations: markets are pricing in five cuts by the end of 2026. For the dollar to recover some of its lost ground, the Fed would need to underdeliver on those cuts – a plausible scenario, given everything we have discussed earlier.

A clear beneficiary of a weaker dollar has been gold. Its rally has been nothing short of spectacular (YTD: +60% as of this writing) and seemingly unstoppable. However, we fear the market may now be entering euphoric territory; a pullback appears both likely and, arguably, healthy. In the longer term, gold remains an excellent hedge against fiscal excess, mounting debt, and monetary overreach.

Beyond the yellow metal, we would avoid oil – except as a tactical hedge against geopolitical shocks – as supply is likely to exceed demand for the foreseeable future. Conversely, the ongoing manufacturing recovery could lend support to industrial metals, provided China avoids a hard landing.[1]

[1] Document sources: LFGZEST, mrb, Capital Economics, BCA, 3Fourteen Research, Creditsight, Empirical, Vontobel, Factset, Refinitiv IBES, Hussman Strategic Advisors, Yardeni, Bloomberg.

About the author

LFG+ZEST SA