“I owe my success to having listened respectfully to the very best advice, and then going away and doing the exact opposite.” – Gilbert K. Chesterton, British Writer

ECONOMY: UPSIDE-DOWN

The year has turned, and as always, major players in the financial industry have rushed to publish their 2026 Outlooks. It is a bit like the January sales. Back in the day, at least here in Europe, they would start on January 6th. Nowadays, you can purchase your Christmas gifts already on sale. Companies rush to lower their prices earlier and earlier to increase their share of Christmas spending. Similarly, financial institutions, research firms, and the like start publishing their next-year outlooks as early as November. I’d say forecasting is almost impossible; at least give yourself a chance and stay close to the forecasting period, at the very least.

As our readers know by now, we do not believe in New Year outlooks; the economy does not go on holiday, nor do the effects of current monetary and fiscal policies, the deterioration in population growth, or any other impactful event that has occurred in the past and whose effects continue through time. Hence, we simply pick up the discussion where we left off last time, namely expressing our doubts regarding the ongoing fiscal and monetary stimulus that the U.S. administration and the Federal Reserve (Fed) are currently injecting into the domestic economy, at a time when the output gap has not yet closed, labor-market normalization following the hiring spree after the pandemic seems to have stabilized, and the outlook for inflation remains uncertain.

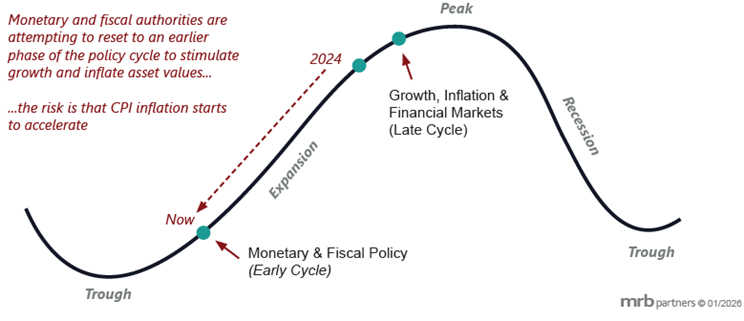

The graph to the right is a good starting point for the discussion; from the standpoint of growth, inflation, and financial asset values, we are currently sitting close to the peak – the green dot on the far right. Monetary and fiscal policies have always been restrictive in this part of the cycle to allow the economy to cool, the output gap to revert, inflation to return to target, and the labor market to loosen. Yet monetary and fiscal policies are calibrated to achieve the opposite; the Fed has been cutting rates from a peak of 5.5% to the current 3.75% and may cut a further 50 basis points by year-end. The elephant in the room may be the new Fed Chair, who will be announced shortly and will take the helm of the central bank in May; there is a high probability that he will want to please the U.S. administration by easing more than currently expected by financial markets. Similarly, as things stand today, the One Big Beautiful Act (OBBA) is set to deepen the federal government’s fiscal deficit further, although forecasts for the medium term are more difficult to draft given the uncertainty surrounding the impact tariffs could have on public revenues. Admittedly, over the last couple of semesters we have seen some signs of cooling in certain areas of the economy but, in our humble opinion, not enough to justify the current stimulative stance of both the Fed and the government.

To reinforce this argument, we note that the U.S. economy is showing improvements in manufacturing as various leading indicators are picking up pace; not only does the current level signal expansion, but the trend has been positive as well. The same is true for most of the global economy, with leading indicators largely in the green area. Recession probabilities are close to zero according to several pundits (including our internal model), and the global economy is on solid footing and appears to be accelerating. The housing market, a major contributor to overall economic growth, has not plummeted under the pressure exerted by higher mortgage rates. Affordability problems for first-time buyers persist because mortgage rates are too high, as are house prices, relative to current household income. However, the large inventory of homes is capping price increases and may eventually begin to push prices marginally lower. The combination of stable to mildly declining prices and stable long-term rates may stimulate housing activity, albeit at low levels. Existing home sales are also improving modestly. Multifamily housing and commercial real estate remain the problematic areas, particularly for regional banks.

Speaking of affordability, consumers continue to spend in line with, or slightly more than, their income growth. This phenomenon – called dissaving – is propelling U.S. economic growth and is bound to last until either prices become too high or income growth stalls. The latter is currently normalizing toward a non-inflationary level, i.e., 3.5-4.0%, still enough to support consumption, especially while financial assets remain buoyant, driving a positive wealth effect. Unfortunately, wealth inequality remains; the top decile of the income distribution, representing 40% to 50% of discretionary spending, is doing well, but how much pent-up demand is left is unknown and, in our view, not much. The remaining segments of the population, especially lower-income earners, are pulling the brakes. For them, monetary and fiscal stimulus are clearly positive, but how effective these measures are for this portion of the population remains unclear. Fortunately, banks’ willingness to lend, alongside a lighter regulatory burden, is improving, which provides a safety net.

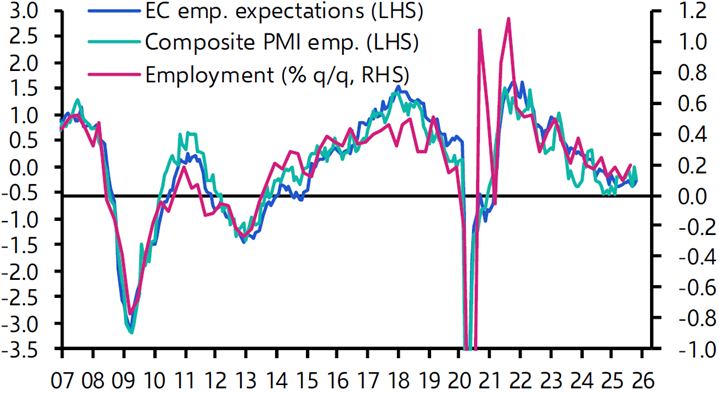

Regarding the job market, as anticipated earlier, we see the Job Openings and Labor Turnover Survey (JOLTS) having normalized at lower levels for this economic expansion but still corresponding to the highs of previous cycles (pre-COVID), suggesting a healthy labor market. We believe that as long as corporate margins remain elevated, similarly to deficit spending, job cuts may be delayed. On the other hand, uncertainty regarding the effects on economic growth of the expansionary fiscal policies that many governments globally are deploying, as well as the advent of artificial intelligence, is visible in the ratio of jobs considered hard to get versus jobs plentiful, and in the hiring intentions of small companies, both of which are deteriorating and thus represent reasons for concern.

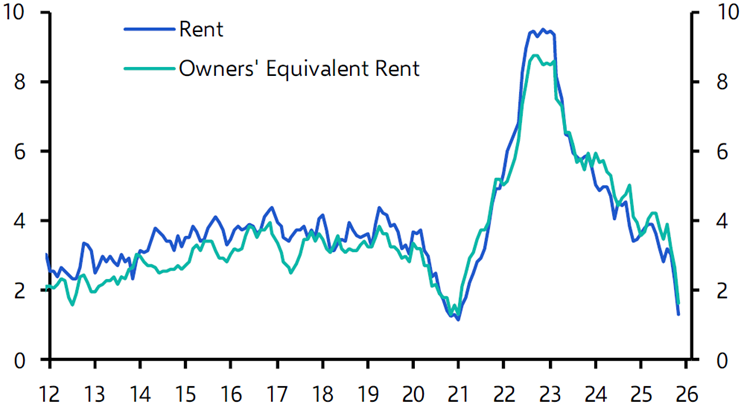

Once again, in our view, inflation may tip the scales. Why is inflation so important? Because it determines the level and direction of interest rates. Moreover, any negative surprise could cause a shock to equity markets, especially at a time when the latter are characterized by high valuations. Presently, inflation has stabilized below 3.0% but remains above the central bank target. Positive factors include expectations of lower oil prices (especially with a resolution in Iran), the normalization of owners’ equivalent rent, and mildly declining house prices in some states. On the contrary, high deficit spending, especially alongside a positive output gap, is pushing in the opposite direction. It is interesting to note that, all else equal, if the rate of growth in rent inflation were to drop near 0%, CPI would converge toward 1.3%. In the short term, we expect uncertainty to dominate, in light of the change in Fed leadership, tariff pass-through, and economic momentum. In the longer term, we see scope for inflation to fall, especially due to lower oil and house prices, two major determinants of the overall CPI level. Therefore, we believe that in the near future the risks are skewed to the upside for both inflation and interest rates, as the economy may pick up given the significant stimulus it is being subjected to and recession risks are low to non-existent.

The 25% appreciation of the euro against the U.S. dollar since the lows reached during the last quarter of 2022 has prompted many commentators to foresee a slowing of the European economy. This has not happened. On the contrary, most European economies are showing positive and improving leading indicators, and 80% of eurozone countries have registered improvements in manufacturing PMIs thanks to fiscal impulses from defense and infrastructure spending. It is true that defense spending has a very small multiplier for the rest of the economy, and that a widening fiscal deficit may coincide with an increase in the region’s debt-to-GDP ratio, but with service economies in the periphery continuing to show resilience, it was one of those “now-or-never” moments. While inflation may gradually trend lower – supported by a strong currency, which makes imported goods cheaper – the European Central Bank (ECB) has paused cutting interest rates, but we believe the next move is more likely to be a cut rather than a hike; growth is below potential, the labor market is softening, and hiring expectations are tepid. With the euro extremely strong, maintaining the current Goldilocks-like environment requires lower rates for the interest-rate-sensitive parts of the economy. A similar fate awaits Switzerland; the extremely strong Swiss franc is weighing heavily on the economy. Many industries can compensate for currency strength by raising the prices of niche products, but this is not true for the financial sector; here, services are largely homogeneous, and with most assets denominated in currencies other than the Swiss franc, revenues are subject to very unattractive conversion rates. Because Swiss inflation is close to zero, the probability that the Swiss National Bank (SNB) will push the reference rate into negative territory is rising.

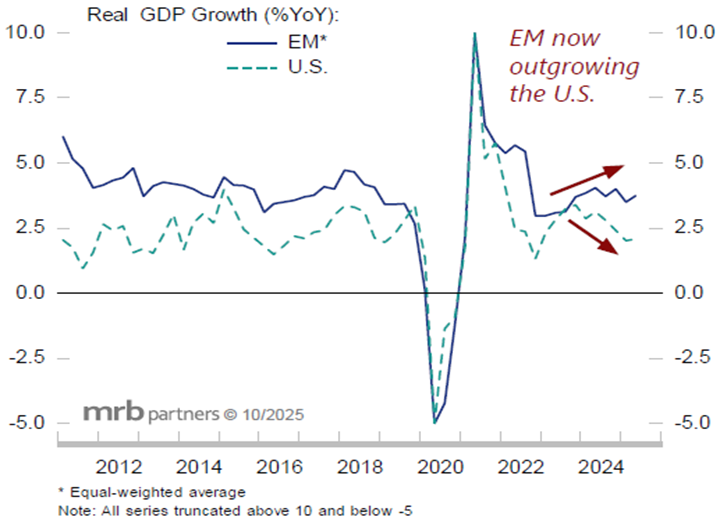

Our concluding remarks are reserved for emerging markets (EM), which staged a strong comeback in 2025, favored by the slump in the U.S. dollar. EM GDP growth has firmed recently, suggesting that the improvement is broad-based (with a few exceptions). For all the talk about the U.S. narrowing its trade deficit with major trading partners, its deficit with EM (excluding China) has widened substantially this year. We believe that tariff exemptions, a lack of domestic alternatives, and a pickup in the U.S. economy may keep demand for EM goods robust.

Yet EM cannot be treated as a single bloc, as was the case years ago. China, for example, is a story of its own, and one that must be told, as it remains the second-largest economy after the United States. In the short term, the EM renaissance may help the Chinese economy muddle through, with demand for many Chinese products on the rise. In the long term, however, we maintain the view that the Chinese economy may be weighed down by the damage the one-child policy has inflicted on population growth. The population began to shrink a few years ago, and such structural trends are hardly reversible. Moreover, with real estate still under pressure, Chinese households are reluctant to spend – and no amount of fiscal stimulus may change this – leaving the domestic economy in a balance-sheet recession.

FIXED INCOME: DURATION RISK

Our stance toward the asset class remains unchanged. As often outlined in the past, almost anything that is not a risk-free asset appears overvalued or, to some degree, expensive. Admittedly, the reassuring global economic outlook makes us more constructive on riskier assets and, contrary to the past, we regard the absolute yields of both high-yield bonds and emerging market issues as attractive. On the other hand, valuations keep us on high alert, conscious that any negative surprise could profoundly affect the future returns of lower-credit investments.

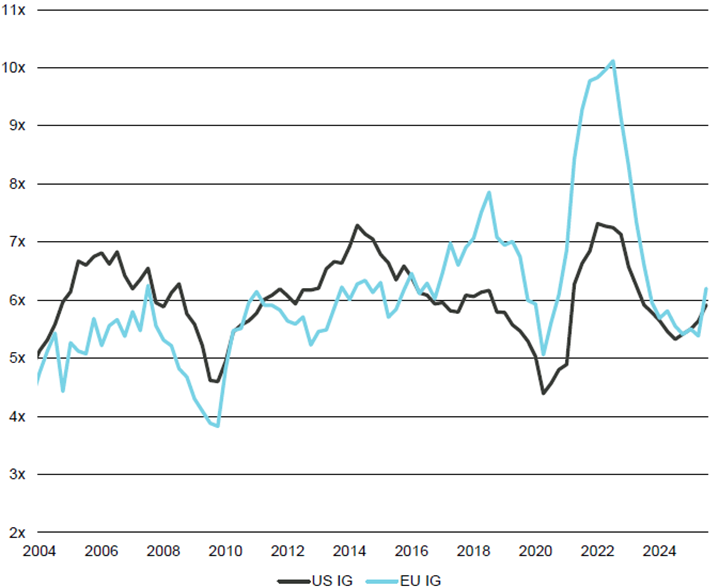

Companies operating in the investment-grade segment of the market remain highly profitable, with strong – and improving – balance sheets, and offer a starting yield that is attractive from a historical perspective. Conversely, lower-credit companies (including those in emerging markets), while benefiting from positive global economic momentum and higher expected returns, have continued to witness net rating downgrades (the number of upgrades less the number of downgrades remains negative), highlighting that higher interest rates and lower oil prices (the energy sector represents more than 10% of the high-yield market) are, on average, denting the balance sheets of companies operating in this space. For these reasons, we still believe that, on a relative basis, higher-quality bonds offer a better risk-adjusted return compared to riskier investments.

Subordinated debt has also been an area that we have often considered very attractive. Here too, however, the yield compression witnessed over the last twelve months has altered the risk-adjusted profile of the asset class, leaving investors wondering whether the juice is worth the squeeze.

Lastly, a word on duration. We are currently experiencing, more or less globally, a steepening of the yield curves, whereby the short end is falling while the long end is rising (and the ultra-long end even more so). Because of the macroeconomic risks highlighted earlier, we caution investors against taking extremely long-duration bets; as we saw during Liberation Day, when the bond market feels that fiscal discipline is being neglected, interest rates can very quickly take unwarranted paths, turning even safer investments into a nightmare one wishes to wake up from rather quickly.

In the short term, we expect uncertainty to dominate, in light of the change in Fed leadership, tariff pass-through, and economic momentum.

EQUITY: FUNDAMENTALLY STRONG

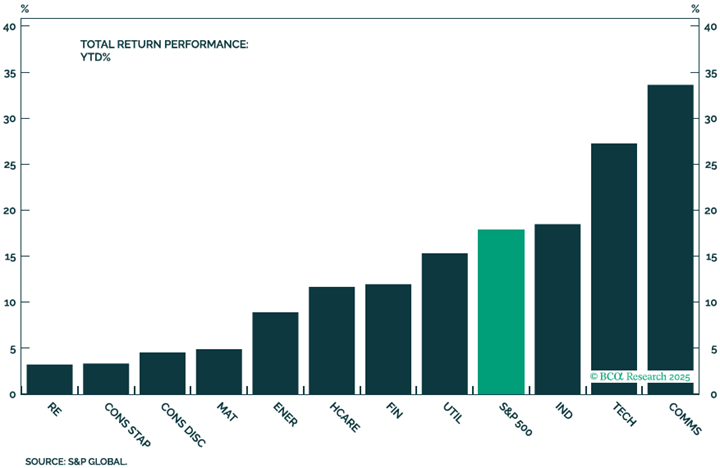

In 2025, communications and technology were the only sectors that meaningfully outperformed the market. As a reminder, today more than 40% of the S&P 500’s market capitalization is represented by only ten stocks. To top it off, most of them are concentrated on a single theme, either directly or indirectly: the boom in artificial intelligence. Hence, the expectation that earnings growth may broaden across more industries – especially more cyclical sectors – is very welcome and could soften the risks associated with a highly concentrated equity market.

The improving economic outlook is supportive of earnings growth, and the third-quarter earnings season was a case in point. Earnings rose a remarkable 11.6% year over year, while sales increased 8.2%, exceeding the 6.9% and 4.8% expected at the start of the quarter. This represents a modest acceleration from the second quarter but, most importantly, it showed an increase in breadth, with 9 of the 11 sectors posting positive earnings growth. Strong earnings momentum is likely to continue well into 2026; 58% of S&P 500 companies issued positive guidance, resulting in S&P 500 earnings expected to grow by 13.3% over the next twelve months. Technology and media companies may lead the way once more, although expectations are already very high for these two cohorts, raising the bar for positive surprises.

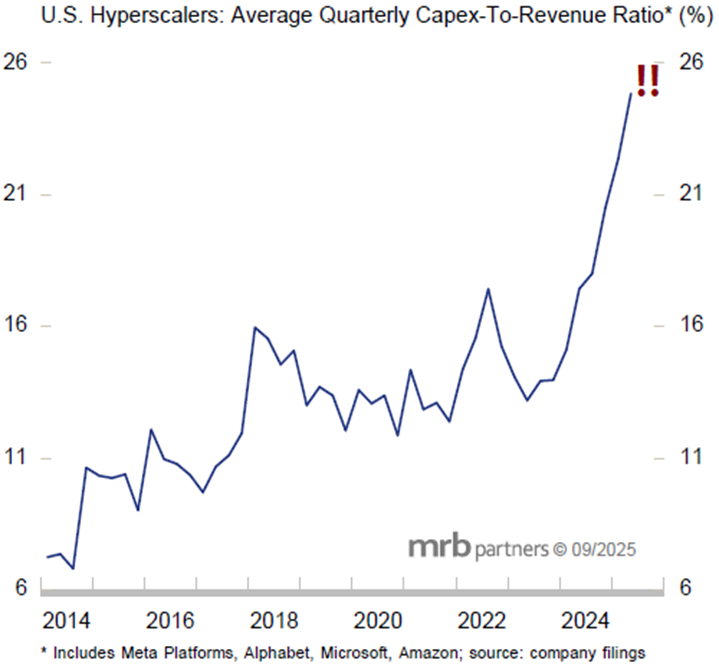

Spending by those players seeking to benefit from the artificial intelligence theme has continued at a massive pace. Microsoft, Amazon, Alphabet, and Meta Platforms, once asset-light businesses, have become more capital-intensive due to their large and growing investments in data centers. The structural increase in the capital intensity of the hyperscalers puts their earnings at greater risk from negative operating leverage should their revenue growth slow. Thankfully, balance sheets remain in extremely good health. Net debt relative to GDP is at its lowest level since the mid-1980s, and during the first half of 2025, net interest and miscellaneous expenses represented just 1.4% of nonfinancial sector debt outstanding, the lowest level since at least the early 1950s. Ergo, exceptionally high spending, even combined with potentially lower earnings, can be sustained from a corporate health perspective; whether equity investors appreciate this, is a totally different story.

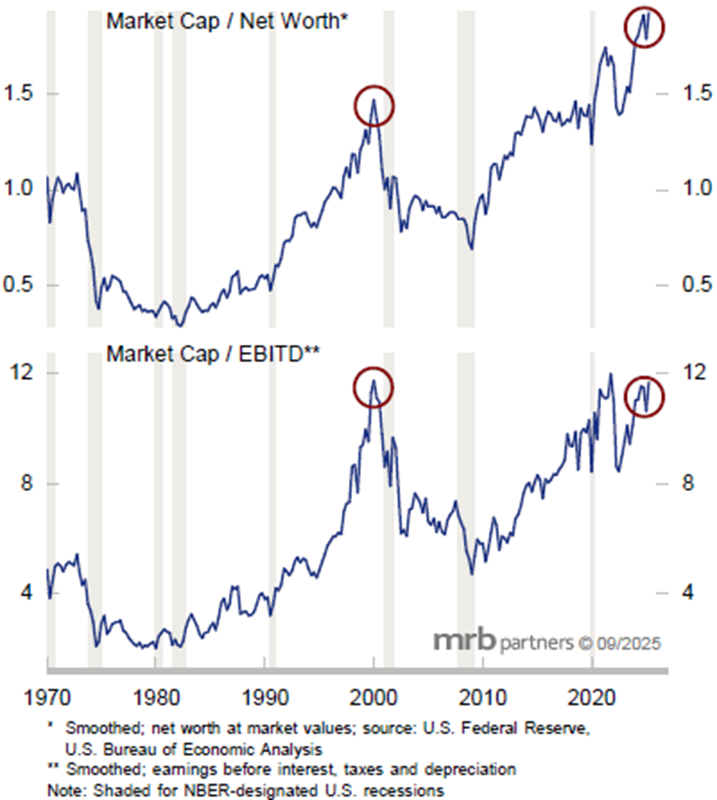

To be fair, being exposed to a handful of stocks is not entirely negative; should the artificial intelligence theme continue to produce outstanding results, the S&P 500 is set to make new all-time highs, ceteris paribus, with the earnings outlook playing in its favor. Therefore, what can go wrong, aside from the risks associated with a highly concentrated market? Similarly to what we have written about fixed income investments, the major risk is represented by stretched – and expensive – valuations, which represent a heavy burden for long-term returns (less so for short-term forecasting). The forward multiple has increased since the market bottomed in April and is now back to the highs reached during the pandemic. Other valuation measures point to the same conclusion. This historically rich valuation coincides with elevated cash-flow margins, signaling outsized potential equity risk if the economic outlook were to deteriorate or if interest rates were to rise. The latter brings us back to the initial macroeconomic discussion about the future path of interest rates, where the Fed resumes its rate-cutting cycle in an environment that might, arguably, be better off without it. Hence, until the music stops, keep dancing – but do not lose sight of the exit door.

Europe and emerging markets are two other regions that, from an equity perspective, appear very interesting, albeit for different reasons. The former is benefiting from a stabilization of the macro picture, earnings consolidation, and still-low valuations compared to its American counterparts. Fiscal measures have certainly helped, and domestic demand has improved, making the Old World appear less fragile to external shocks than before. The latter is a clear winner during a prolonged USD depreciation, especially if combined with reaccelerating global economic growth. However, not all animals are equal, as George Orwell wrote. Within emerging markets, selectivity is essential to avoid falling into traps; in the long term, China may be one of them, while Southeast Asia, India, and Mexico exhibit very attractive growth profiles.

CURRENCIES AND COMMODITIES: SAFE-HAVENS VOLATILITY

The current macroeconomic environment, together with expectations of further growth ahead, is clearly positive for cyclical currencies (the Australian dollar, the Norwegian krone, and the like). On the other hand, the monetary and fiscal stimulus the United States is deploying does not bode well for the greenback. Moreover, its valuation remains high despite the pullback experienced over the last eighteen months. Clear beneficiaries of a weaker USD have been — and may continue to be — the euro and the Swiss franc, although the central banks of the two regions are growing visibly uncomfortable with the strength of their currencies and may decide to intervene, either directly or indirectly, to weaken them.

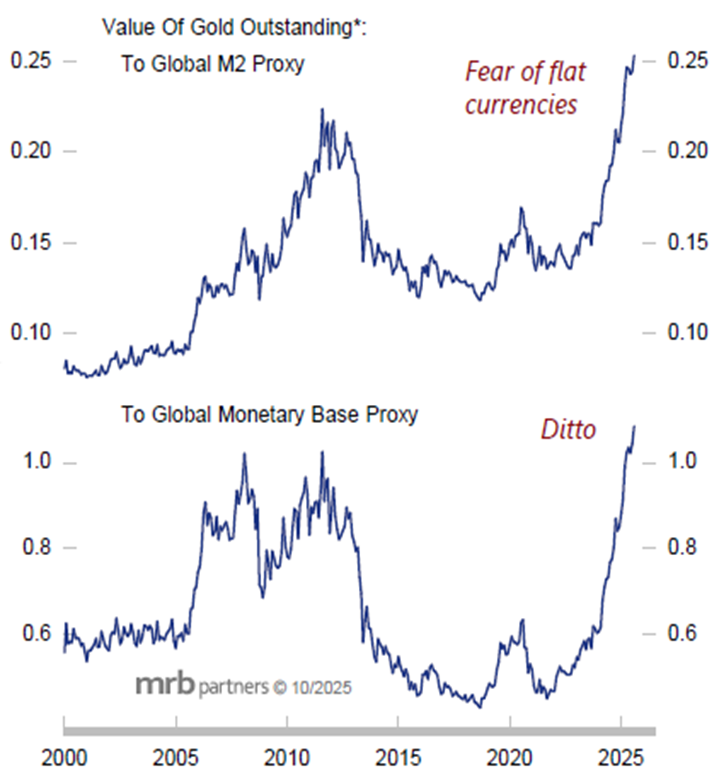

Despite the heightened volatility that has recently characterized precious metals, expectations of a depreciating USD and lower real yields are supportive of gold, notwithstanding valuations that have reached all-time highs. Yes, high valuations are a recurring theme, and much of the reason can be attributed to the excessive liquidity the world has been granted over the past decade. In contrast, oil prices have few reasons to rise; OPEC+ policy remains a dominant factor, although the unwinding of a second tranche of output cuts appears already priced in. Geopolitically, Venezuela’s potential increase in output is not yet fully understood but would be negative for prices, as would a possible resolution in Iran. Lastly, a word on industrial metals, specifically copper: as things stand, demand for copper related to artificial intelligence is not yet impactful (around 2% of total), while China’s property crisis weighs on overall demand. Supply may be constrained due to a string of mine supply shocks that took place in 2025, but this also appears largely priced in. Conclusion: do not expect much from copper prices in 2026, barring market speculation.[1]

[1] Document sources: LFGZEST, mrb, Capital Economics, BCA, 3Fourteen Research, Creditsight, Empirical, Vontobel, Factset, Refinitiv IBES, Hussman Strategic Advisors, Yardeni, Bloomberg.

About the author

LFG+ZEST SA