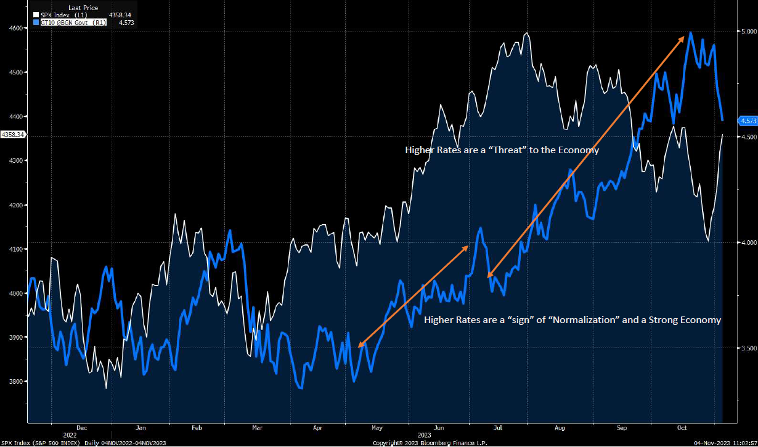

The movement of the stock market over the past three months is mainly explained by the change in the US 10-year interest rate. The reason is the use of the 10-year US interest rate within many quantitative models to estimate the fair value of shares. The two variables are inversely proportional.

As can be seen from Chart 1, from May to July, the two elements moved, unusually, in the same direction. A sign of the resilience of the economy and the stable balance sheets of companies and households. When rates started to bite into the economy, threatening the status quo and growth prospects, the stock market corrected.

The main reason for the interest rate movement is the steep rise of the term premium. The term premium is the compensation required by the investor to hold long-dated bonds, which incorporate greater unknowns associated with economic and financial factors.

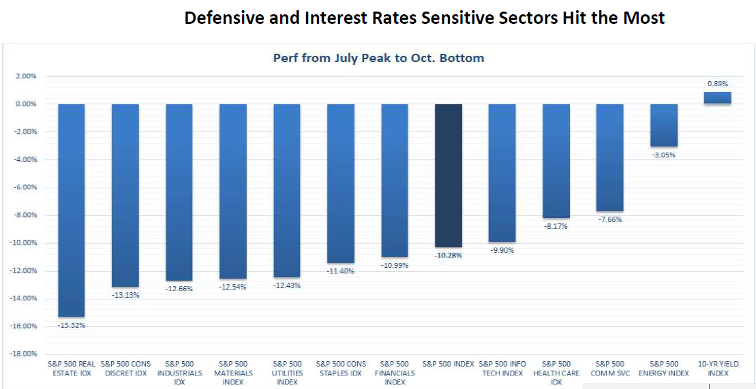

Analysing the performance of individual sectors from the July peak to the October bottom, we noticed something unusual: sectors generally defined as 'defensive' (i.e., Utilities and Consumer Staples), characterised by 'low beta' (it measures the expected change in a stock's return for every one percentage point change in market return), did not behave as such. On average, they lost 1.5% more than the S&P500 (Chart 2).

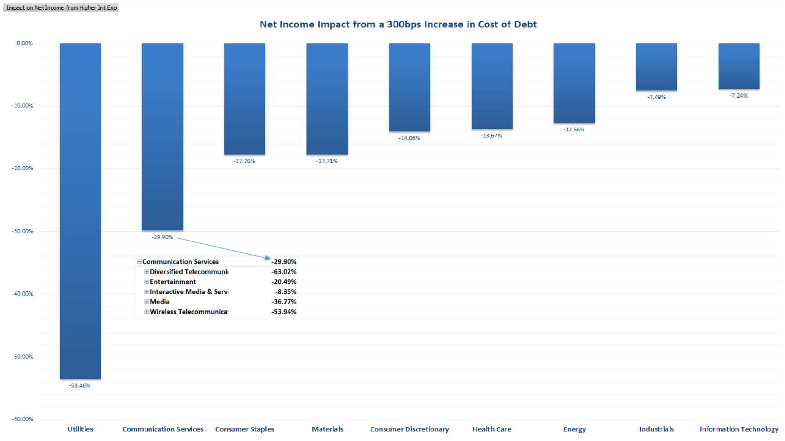

This can be explained by the exposure to changing interest rates of the underlying companies' balance sheets. We assumed that in two years’ time all companies in the S&P would have to refinance themselves at current rates. Companies within the defensive sectors are the ones that would be most negatively impacted (Chart 3).

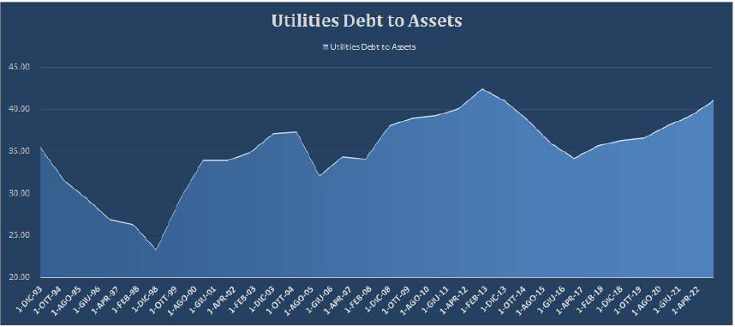

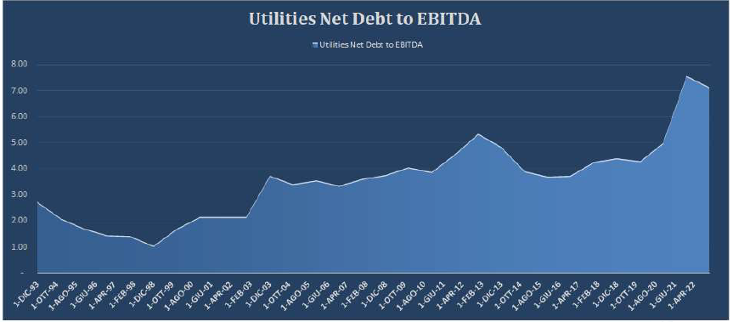

The reason is the growth of debt over the last few years. Taking the example of Utilities, a strong growth in both "Debt to Assets" (Chart 4) and "Net Debt to EBITDA" (Chart 5) ratios is evident from the graphs below. This confirms that the sector is less efficient than in the past.

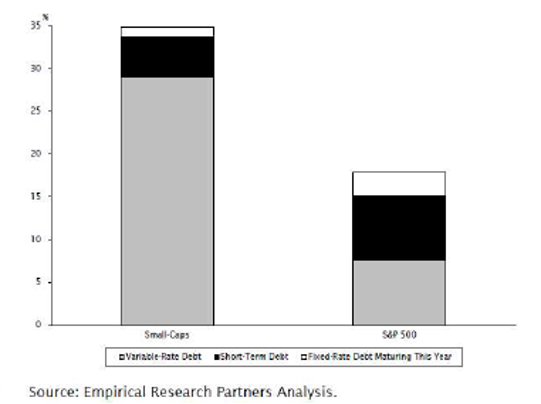

Another segment of the stock market that has been heavily affected by rising rates is the small cap sector. The cause is to be found in the exposure to variable rate borrowing, which is the preferred measure used by small-cap companies. Chart 6 shows the percentage of small-caps exposed to variable-rate debt compared to similar companies in the S&P500.

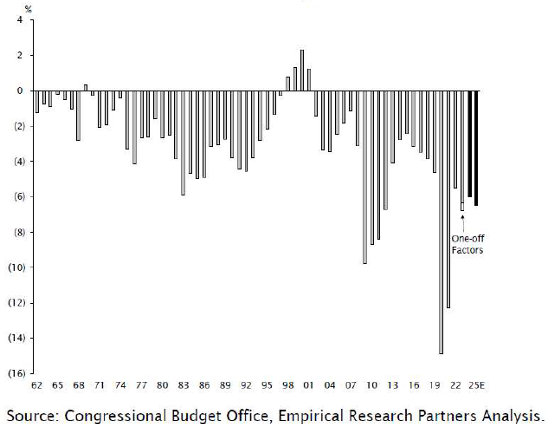

The sharp rise in interest rates over the past year has changed the market status quo and we will most likely never return to a 0%-rate world. This thesis is also supported by the US government's fiscal indiscipline. In recent years, US government spending has been heavily financed by deficits. CBO (Congressional Budget Office) estimates that the annual deficit will be 6.1% until 2030 (Chart 7).

This behaviour will lead to medium/long-term interest rates remaining higher. As a result, the cost of interest on the debt will be higher and the U.S. government could raise taxes to lessen the impact on the public budget.

Currently, the tax paid by domestic companies is about 38%, while that of global companies is much lower. As an example, Apple pays about 17%. This is because global companies move their headquarters to countries where taxation is more favourable.

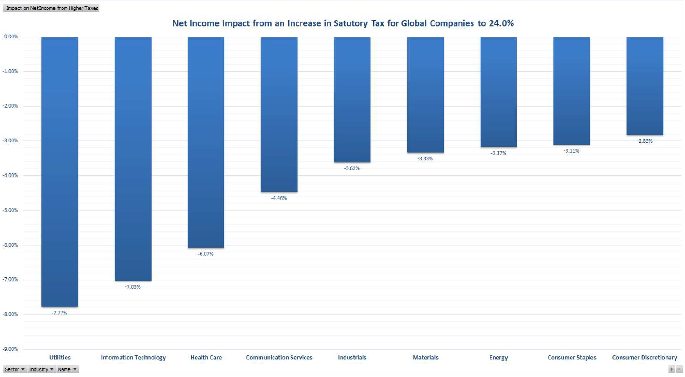

We performed an analysis in which we assumed a tax hike for global companies to 24%. The impact on Net Income would be most significant on corporations belonging to Utilities, IT and the Health Care sector (Chart 8). The reduction would be 6/7%, important, but not too severe.

Short-Term and Medium-Term Outlook

To conclude we show two charts summarising our view of the stock market in the short and medium/long term.

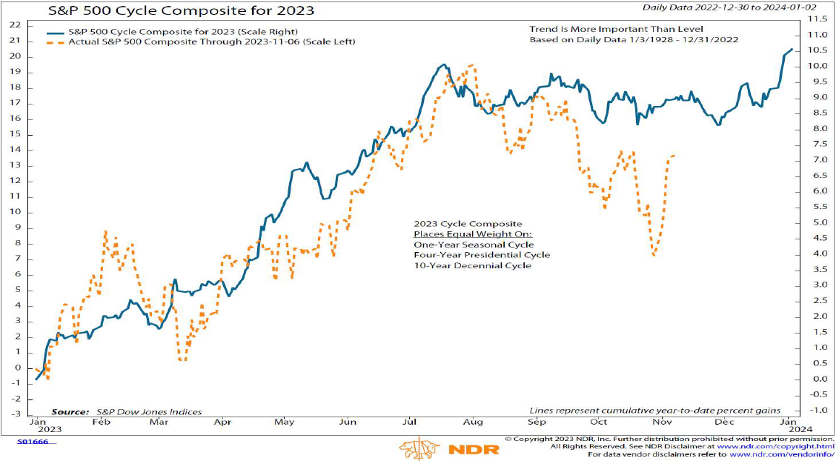

Starting from the short-term, the blue line in Graph 9 shows the cycle of the S&P 500 in 2023 through an average of 1yr seasonal cycle, 4yr presidential cycle e 10yr cycle (equal weight). In orange, the performance of the S&P 500 to date. We are entering the most solid period of the year, thus a continuation of the current rally is plausible.

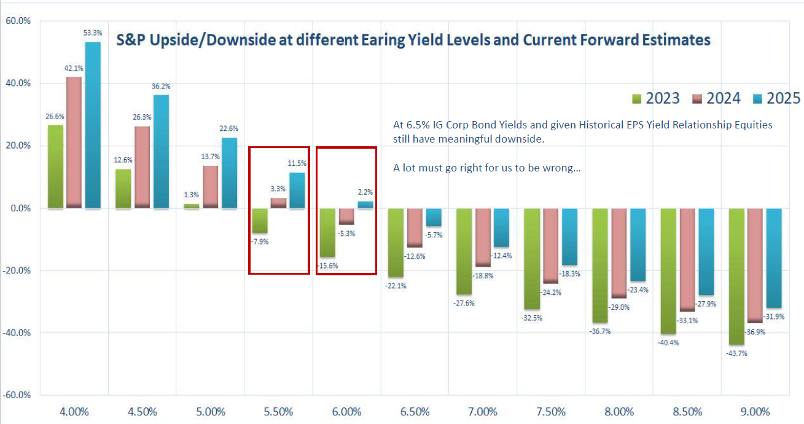

On the other hand, in the medium/long term our outlook remains unchanged. Today, with Corporate Bond Yields around 6%, equity investors are not adequately compensated. The S&P 500 Earning Yield is around 5%, while it should be at least at 6% to make the stock market attractive. Nevertheless, Chart 10 shows that assuming an earning yield at 6%, with current earnings estimates, there is no room for a potential upside of the S&P 500 in either 2023 or 2024.

About the author

LFG+ZEST SA