INVESTMENT INSIGHTS: IN THE MIDST OF A TRANSITION PHASE

“You are so past the line that you can’t even see the line! The line is a dot to you!” – Matt LeBlanc (Friends), actor

ECONOMY: TRANSITIONING

Phase transitions. More or less what we think is currently happening in the US economy. Phase transitions is a term often used in chemistry (but not exclusively there) to describe the transformation of a substance from one state to another. We have read this term often during the recent past, and we find it very useful to illustrate the transformation the US economy is experiencing.

Take water, for example. If you wish to turn water into ice, all you need to do is place the container holding the water into the freezer (possibly, not a container made from glass, otherwise you will find yourself with one piece less of tableware) and wait until the water turns into ice. You don’t need to change the temperature of the freezer; if it stays below zero degrees Celsius, the water will eventually turn into ice. You can certainly speed up the process by lowering the temperature, or you can slow it down by increasing the temperature. But as long as it remains below zero, it will definitely turn into ice.

The economy is your water, and the temperature inside the freezer is your interest rate level. The fact that for more than two years (March 2022, when the Federal Reserve – the FED – first raised interest rates) the economy has fared well despite rising interest rates, does not mean that the water is not turning into ice. You just don’t see it. More importantly, you don’t need to lower the temperature (i.e. increase interest rates) for the water to freeze (i.e. for the economy to suffer a recession). It’s most likely only a matter of time. Phase transition, precisely.

Indeed, while water will always turn into ice if placed for enough time below zero degrees Celsius, an economy will not necessarily always fall into a recession if interest rates are kept at elevated levels for a prolonged period. Yet, the odds are not in our favour, and the second quarter has provided little evidence that this time should be any different, despite what the satisfactory returns of financial markets may prompt us to think.

By no means do we want to be presumptuous, nor do we believe we are unquestionably correct in our view; after all, if financial markets (i.e. the consensus) believe in a soft-landing, then one might conclude it is the most probable outcome. Nonetheless, recent economic data suggests that cracks are indeed forming into the US economy, specifically among low-income consumers and within both the labour market and parts of the real estate market.

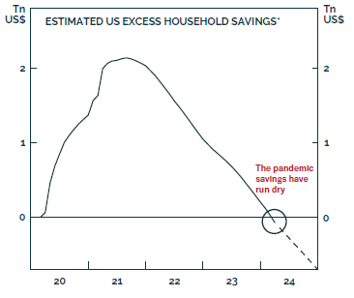

The depletion of US household excess savings (chart I) will force consumers to save more, at a time when wage growth is normalizing and credit availability is limited due to tighter lending standards by banks, leading to a reduction in consumption. As a result, the growth in real retail sales has been negative for some time while delinquency rates on household debts are rising and could become concerning by the fall. On the other hand, the top quintile of income distribution, representing 40% of discretionary spending, is doing well, but how much pent-up demand remains is unknown, and their marginal propensity to spend is low (i.e. becoming richer doesn’t make this segment of the population spend more). As long as interest rates remain elevated, we expect consumers to freeze their spending.

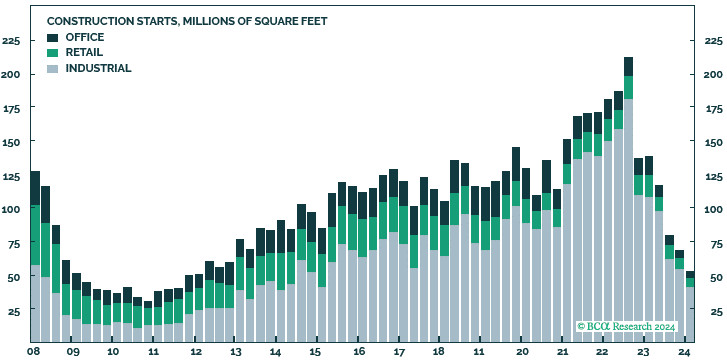

Elevated interest rates are also having negative effects on the real estate market. We have often talked about the issues surrounding commercial real estate, thus we won’t spend further time on this. Suffice it to say is that the positive stimulus from the Chips Act and the Inflation Reduction Act is now over (chart II). The housing market presents contradictory evidence; single-family homes continue to be undersupplied, while cracks are building in the multi-family market, as oversupply is leading to a slowdown in transactions. Moreover, many homeowners are unwilling to switch properties because it would entail entering a new, much more expensive mortgage. Because the housing market represents a big source of economic growth, we expect the current slowdown to have material effects on the overall economy, starting from the labour market.

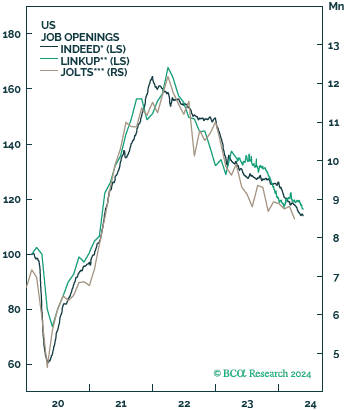

Indeed, what the last quarter told us is that the labour market has begun to soften. The unemployment rate has moved from a low of 3.4% in January ’23, to the 4.1% released in June of this year. More worrying is that it has risen constantly over the past three months (from 3.8% to 4.1%). Simultaneously, the number of temporary workers is plummeting. Why is this important? Because firms tend to fire temporary workers before they begin to cut full-time employees. History shows that when the unemployment rate begins to rise, it tends to self-perpetuate, as job losses bring lower consumption, which in turns brings more job losses. A confirmation of the deterioration of the labour market comes as well from the demand-side of the equation; the recent number of new hires have been lacklustre, when excluding those that were appointed in public offices and in the health care sector. Similarly, the job openings rate (and similar indicators such as the hiring rate and the quits rate) all point to the same, gloomy direction (chart III).

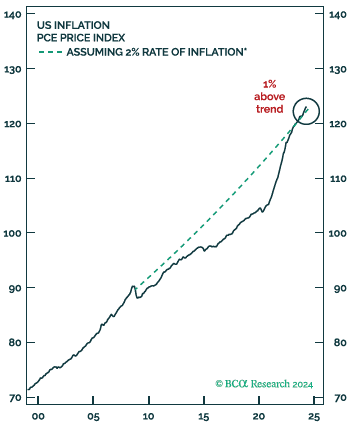

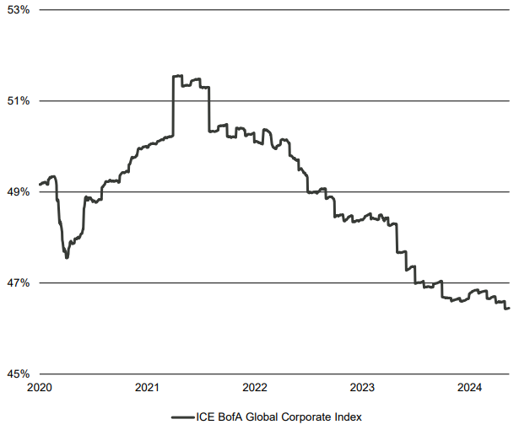

Cooling consumption, cracks widening in the real estate market, and a weakening labour market; we have all the ingredients necessary for the FED to start cutting rates aggressively. Yet, the central bank is hesitant. The source of this impasse is once again the fear that cutting interest rates too early will unleash a second wave of inflation. While years of subdued inflation compensated the spike we have experienced over the recent past, we are now back on the long-term trend and thus, above-average inflation would risk unanchoring long-term inflation expectations, with the spectre of the 1970s lingering within the walls of the Marriner S. Eccles Building (chart IV).

The good news is that inflation, after a surprisingly strong beginning of the year, is now relentlessly falling towards the FED target. With respect to the previous quarter, we are more confident prices will continue to fall over the coming months, as “catch-up” items are about to kick-in. For example, the new tenant rent growth rate is almost zero, which will trim the average rent growth rate, as existing contracts expire and are renewed at lower prices.

Unfortunately, the good news end here. For us, a recession is a non-zero probability event. While we don’t expect something similar to the one experienced during the great financial crisis, our mood is in stark contrast with the growing optimism among CEOs that a recession can be avoided. With a slowing economy, and the FED unable to cut aggressively, the only other white knight out there is a possible fiscal stimulus from the government. However, considering the (delicate?) state of the US government balance sheet, it is highly unlikely it will be able to come to the rescue. If anything, the chances are that the need to reduce the budget deficit will be a detractor to economic growth going forward. We hope to be wrong, but the numbers are currently pointing to the water freezing. We are in the midst of a phase transition.

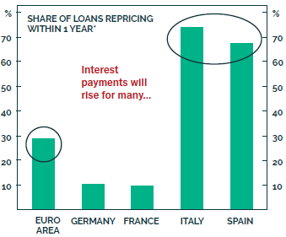

The rest of the world isn’t faring much better. Europe and Japan plod along, as GDP growth is stagnant. In Europe, unemployment is low, but on the rise, while inflation is falling (more so in Europe than in Japan). As China continues to struggle with a shaky economy and given the US may enter a mild recession soon, it is highly likely the European economy will follow suit. For these reasons, in June, the European Central Bank (ECB) has cut the reference rate, but it has clarified that this is not necessarily the beginning of a rate-cutting cycle. Inflation is still higher than the target, and the labour market is still strong. Thus, the ECB remains highly data-dependent. Yet, we are convinced that the governing council is well-aware of the amount of debt that needs to be refinanced over the course of the next twelve months; 30% for the Euro area, with Italy and Spain reaching peaks of 70% (chart V). Thus, our two cents is that the path to normalization has just begun.

On the other hand, the Bank of Japan is under pressure to increase interest rates – the first hike took place in March of this year, ending a 10-year period of negative interest rates. But this is not enough. With inflation running close to 3% and a tumbling domestic currency (the JPY has lost more than 50% against the dollar since the start of the FED hiking cycle), the central bank is obliged to do more.

Our concluding remarks are reserved for the Chinese economy, which has indeed rebounded during the first months of the year, supported primarily by the services sector. However, rather than internal demand (as the government targets), it was the export of goods (specifically, electric vehicles - EVs) that stimulated the economy. Given the congestion at European ports, we can assume the rise in exports will not last, and what we are left with are the recurring issues in the domestic housing market, a wound that will take years to heal.

FIXED INCOME: ADOPT A LONG-TERM VIEW

The prospect of a deteriorating global economy makes, in our view, the current level of interest rates an attractive entry point for long-term investors. The big elephant in the room is a possible election of Mr. Trump, which could destabilize the bond market, at least in the short-term, if he really implements the fiscal policies he is advertising.

Broadly speaking, credit spreads of both investment grade and high yield issuers are unattractive, and don’t repay the investors for the risks they expose themselves to. However, while on average investment grade issuers have witnessed a constant improvement in their balance sheet metrices, justifying current bond prices, high yield issuers’ balance sheets have been deteriorating, confirmed by the constant rise in the default rate over the past few years. This is also reflected in the number of upgrades/downgrades since the start of the year; while within high-quality issuers the ratio points to an improvement of the credit conditions, the opposite is true for lower-quality issuers, where the number of downgrades continues to outpace that of the upgrades. Thus, at the risk of boring you, we reiterate our preference for government and high-quality issuers.

Remaining in the riskier segment of the fixed income market, we note that emerging markets bonds have had an incredible rally, riding the risk-on phase that has characterized financial markets since the fourth quarter of 2023. Today, emerging markets bond investors are not compensated for the risk they own, as credit spreads are well below their long-term average. In absolute terms, we still believe the yields offered are attractive, but on a relative basis, we prefer subordinated and/or hybrid issues from investment grade financial and non-financial corporations, which offer higher yields despite having healthier balance sheets, on average.

EQUITY: MARKET BREADTH MISSING

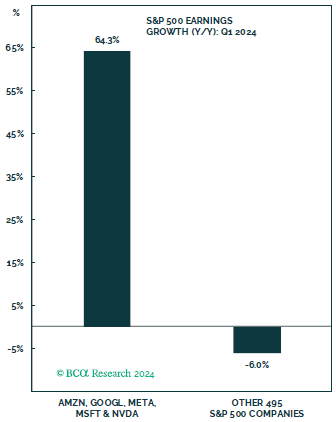

We don’t think we are in a bubble. Nor do we think the current period is anywhere close to what we have experienced during the early 2000s. The information technology sector is an earnings powerhouse, with huge cash balances, on average. But the equity market structure is very weak. The breadth is very low, both in terms of earnings growth and in terms of equity returns. The earnings growth of a handful of companies (the largest ones) compensates for the meagre results of the rest of the market. Consider this: in Q1, the earnings of Amazon, Alphabet, Facebook, Microsoft, and Nvidia grew on aggregate by 64% YoY. The earnings of the other 495 companies contracted by 6% YoY (chart VII). Thus, it is no surprise to see that, at the end of the first semester, the S&P 500 was up 15%, while the S&P 500 Equal Weight was up just 5%. Were these magnificent companies trading at a bargain price, we would be less worried. But these companies trade at valuations that are “so past the line that the line is a dot” to investors. Can this last? Sure. As a long-term investor, should you chase this? Your choice, but we would not.

Speaking of fair valuations, to justify today’s S&P 500 level (5’600), the earnings growth for the next twelve months should come in between 10% and 20%, while valuations should remain close to where they are today (forward price/earnings above 23x). This should happen in an economic environment that may continue to decelerate. Of course, we could keep witnessing an expansion of the multiple, which would imply the S&P 500 rising from current levels without material earnings growth (this is what happened throughout the first half of this year). On the other hand, it’s worth noting that should we enter a recession, earnings would contract by roughly 10% and the multiple would normalize to roughly 16x (both estimates are conservative by historical standards), leading to a fair value of the S&P 500 of approx. 3’700. This is not to scare anyone. It may never happen, or perhaps it will happen way into the future. But there are downsides risks that positive equity returns are currently hiding from you. We just want to make you aware. Be prudent. The return of a 1-year Treasury is higher than 5%, with no risk. Just saying.

The good news is that inflation, after a surprisingly strong beginning of the year, is now relentlessly falling towards the FED target.

Within an equity exposure, being prudent would mean implementing an allocation to regions that are cheaper compared to the United States (Europe and Switzerland, for example), or taking an exposure to sectors that are less cyclical – i.e. whose earnings are predictable and stable through time – such as health care, consumer staples, utilities, and part of the communication services.

CURRENCIES AND COMMODITIES: KING GOLD

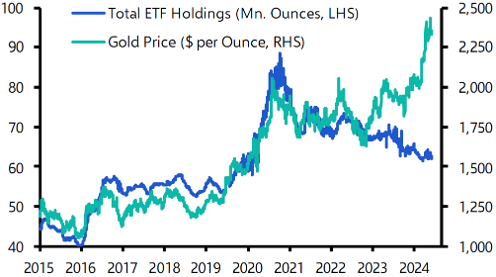

Geopolitical decisions, a stronger dollar, and economic problems in China are all reasons justifying the recent correction in the commodities market. Industrial metals may face some headwinds as the economy slows down, with metals linked to the EV market pressured as the latter suffers from overcapacity and falling demand. On the other hand, precious metals, and gold in particular, remained upbeat despite central banks having diminished their purchases amid very high prices (chart VIII).

With all that has happened, oil prices remained in a range (70$/b – 90$/b) for much of the past two years. Going forward, the outlook for the economy, and the developments in the Middle East are the major factors to focus on. We don’t expect this range to be broken anytime soon, or if it does, not for too long.

The positive trajectory of the interest rate differential is keeping the USD close to its 20-year highs (DXY Index), despite its valuation being expensive. Its countercyclical characteristic should continue supporting its valuation in the near term, especially if the global economy falls into a recession. Over the longer-term, fundamentals should kick-in and the greenback is bound to depreciate, in our view.[1]

[1] Document sources: Capital Economics, BCA, 3Fourteen Research, Creditsight, Empirical, Vontobel, Factset, Refinitiv IBES, Hussman Strategic Advisors, Yardeni, Bloomberg.

About the author

LFG+ZEST SA