On Saturday, February 28, the United States and Israel launched a joint attack against Iran. In the following days, Tehran responded by escalating the conflict and involving several other Gulf countries. This new geopolitical escalation unsettled financial markets, leading to a sharp increase in oil and natural gas prices, while equity markets in countries most exposed to the region’s energy flows came under pressure.

In this analysis, we examine how this conflict fits into the current macroeconomic environment and assess its potential implications for financial markets.

The U.S. economy continues to show signs of resilience. As illustrated in Chart 1, the Services Purchasing Managers’ Index (PMI) is accelerating and remains above the 50 threshold, which separates economic expansion from contraction. At the same time, the manufacturing cycle has also returned to expansion territory, with the index reaching 53.3 at the end of February.

The strength of the U.S. economy, which continues to serve as a key anchor for the global economy, is occurring within an overall accommodative monetary environment. As illustrated in Chart 2, only 10% of central banks worldwide have raised interest rates over the past eight weeks. This implies that the remaining 90% of monetary authorities, in their most recent meetings, have either reduced policy rates or kept them unchanged, effectively maintaining an accommodative monetary stance. Historically, such an environment tends to be supportive for financial markets.

However, these data points and the current stance of central banks may be challenged by the potential impact that this conflict could have on the global economy and financial markets. In particular, the upward shock in oil prices currently observed in the markets could reignite inflationary pressures, potentially triggering a chain reaction as investors reassess their economic outlook and monetary policy expectations. The longer oil prices remain elevated, the greater the likelihood of a meaningful impact on inflation and, consequently, a potential shift in central bank positioning. Monetary authorities have already stated that they are closely monitoring developments and their macroeconomic implications.

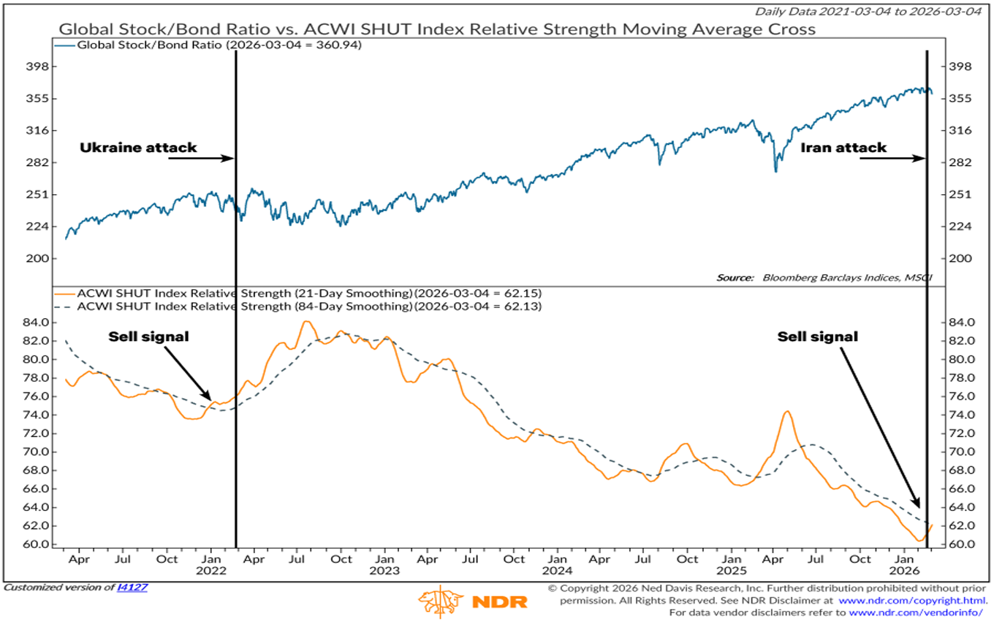

To better understand how such a move in oil prices could affect financial markets, it is useful to look at the market dynamics observed following Russia’s invasion of Ukraine. Chart 3 highlights that in the immediate aftermath of the invasion, high-yield credit spreads widened while global equity markets experienced a period of weakness. Following the attacks involving Iran, a similar pattern could potentially emerge. For this reason, it is important to remain vigilant and closely monitor developments, even though market conditions remain relatively stable for the time being.

A prolonged period of elevated oil prices would likely have a meaningful impact on the economy, affecting the labor market and, consequently, U.S. consumers. Households in the lower income brackets tend to be more sensitive to inflationary shocks, as a larger share of their expenditures is allocated to essential goods, and many are already facing increasing affordability constraints. In this context, a potential mitigating factor could come from the OBBBA (One Big Beautiful Bill Act), which is expected to significantly increase consumers’ disposable income, as illustrated in Chart 4.

Fiscal measures aimed at increasing disposable income have historically supported consumer spending, particularly among lower-income households. Within this segment, a larger share of additional income tends to be directed immediately toward consumption. An additional source of support for consumption could also come from wage growth. The introduction of more restrictive immigration policies by the Trump administration is already having visible effects on the labor market. In an environment characterized by slower labor force growth, fewer new hires will be required to maintain a stable unemployment rate. As a result, employers may increasingly compete to attract qualified workers, offering higher wages in order to secure the most suitable candidates, as illustrated in Chart 5.

The 25% appreciation of the euro against the U.S. dollar since the lows reached during the last quarter of 2022 has prompted many commentators to foresee a slowing of the European economy. This has not happened. On the contrary, most European economies are showing positive and improving leading indicators, and 80% of eurozone countries have registered improvements in manufacturing PMIs thanks to fiscal impulses from defense and infrastructure spending. It is true that defense spending has a very small multiplier for the rest of the economy, and that a widening fiscal deficit may coincide with an increase in the region’s debt-to-GDP ratio, but with service economies in the periphery continuing to show resilience, it was one of those “now-or-never” moments. While inflation may gradually trend lower – supported by a strong currency, which makes imported goods cheaper – the European Central Bank (ECB) has paused cutting interest rates, but we believe the next move is more likely to be a cut rather than a hike; growth is below potential, the labor market is softening, and hiring expectations are tepid. With the euro extremely strong, maintaining the current Goldilocks-like environment requires lower rates for the interest-rate-sensitive parts of the economy. A similar fate awaits Switzerland; the extremely strong Swiss franc is weighing heavily on the economy. Many industries can compensate for currency strength by raising the prices of niche products, but this is not true for the financial sector; here, services are largely homogeneous, and with most assets denominated in currencies other than the Swiss franc, revenues are subject to very unattractive conversion rates. Because Swiss inflation is close to zero, the probability that the Swiss National Bank (SNB) will push the reference rate into negative territory is rising.

Our concluding remarks are reserved for emerging markets (EM), which staged a strong comeback in 2025, favored by the slump in the U.S. dollar. EM GDP growth has firmed recently, suggesting that the improvement is broad-based (with a few exceptions). For all the talk about the U.S. narrowing its trade deficit with major trading partners, its deficit with EM (excluding China) has widened substantially this year. We believe that tariff exemptions, a lack of domestic alternatives, and a pickup in the U.S. economy may keep demand for EM goods robust.

Yet EM cannot be treated as a single bloc, as was the case years ago. China, for example, is a story of its own, and one that must be told, as it remains the second-largest economy after the United States. In the short term, the EM renaissance may help the Chinese economy muddle through, with demand for many Chinese products on the rise. In the long term, however, we maintain the view that the Chinese economy may be weighed down by the damage the one-child policy has inflicted on population growth. The population began to shrink a few years ago, and such structural trends are hardly reversible. Moreover, with real estate still under pressure, Chinese households are reluctant to spend – and no amount of fiscal stimulus may change this – leaving the domestic economy in a balance-sheet recession.

Considering that the earnings yield stood at approximately 4.00% in 2025 and that no clear signs of recession are currently visible, it is reasonable to assume that this indicator could continue to improve over the coming years. In light of the positive earnings revisions highlighted in the previous chart, the earnings yield could rise to around 5.00% by 2027. Such a scenario would suggest a potential upside for the S&P 500 index in the range of approximately 5–7%, as illustrated in Chart 7.

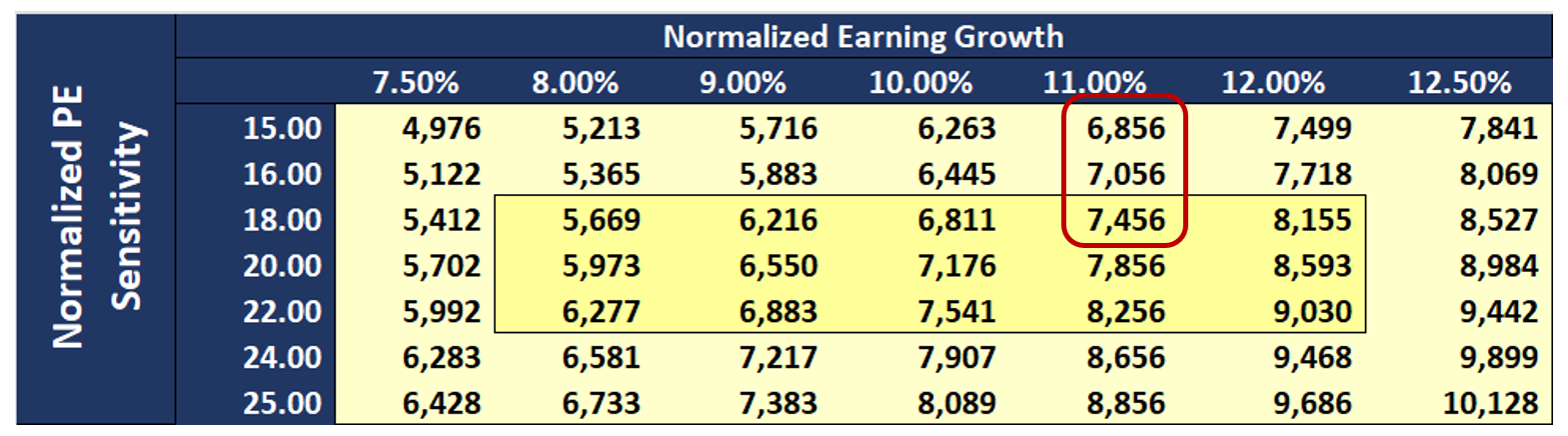

At present, our internal valuation model, based on current real interest rates priced by the market at around 1.30% and an excess nominal earnings growth (defined as nominal earnings growth minus nominal GDP growth) of approximately 3%, in line with the average of the past ten years, leads to the estimates shown in Table 1. Under this framework, corporate earnings could potentially grow by around 11%. This would imply an S&P 500 P/E multiple in the range of 16–17x and a fair value of approximately 7,200 points, suggesting a potential upside of about +6.5–7% in the absence of a recessionary scenario.

Consequently, barring significant disruptions, such as a prolonged period of elevated oil prices or a meaningful deterioration in economic conditions, the outlook for the U.S. equity market remains broadly constructive.

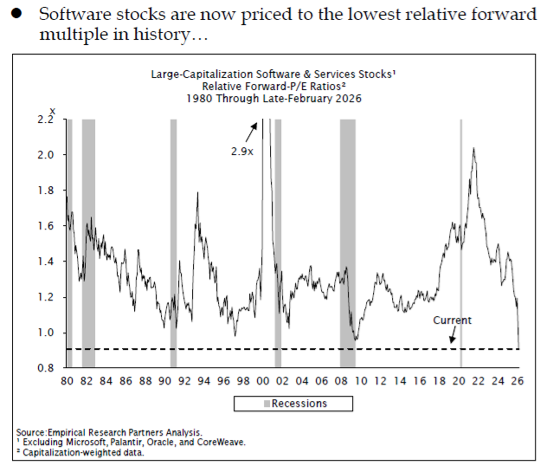

Finally, we provide a brief analysis of the software sector, which has recently been heavily impacted by investor concerns regarding the potential disruption or partial replacement of existing business models as artificial intelligence continues to expand and develop. In particular, Chart 8 highlights the sharp shift in the sector’s forward P/E relative to the broader market. Historically, software companies traded at a premium of roughly two times compared to other companies within the index. However, following a significant derating by investors, the sector is now trading at a discount.

This significant de-rating is clearly illustrated in Chart 9. Most of the data points, each representing an individual software stock, lie below the red bisector, which reflects the growth implied by analysts based on expected revenues over the next two years. This suggests that investors are currently more pessimistic about the sector than analysts’ growth expectations would imply. Should these expectations materialize, the sector could potentially experience a meaningful upward revaluation by the market.

About the author

LFG+ZEST SA