The current phase of the economic cycle shows signs of resilience, but also some elements that require close monitoring. To truly understand where we stand in the cycle, it is essential to look at the broader picture by examining different economic variables, the condition of households and businesses, and structural trends such as demographic dynamics. The following charts help build exactly this comprehensive view.

High-frequency data (Chart 1) indicate that the U.S. economy continues to move with solid momentum: the Dallas Fed’s GDP Now remains stable around 2.5%, Retail Sales maintain a positive trend, and the unemployment rate, although slightly higher, remains well below levels that have historically preceded a recession.

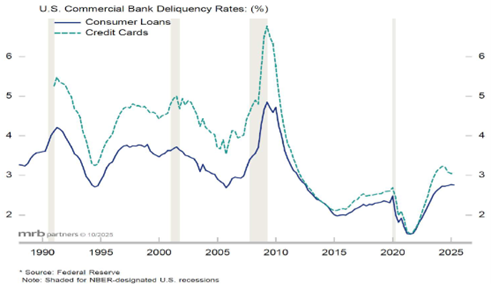

However, some vulnerabilities are beginning to emerge. Chart 2 highlights the fragility of lower-income households, which are starting to struggle with repayments on credit-card balances and auto loans. The situation, however, remains under control: default rates are still at historically low levels.

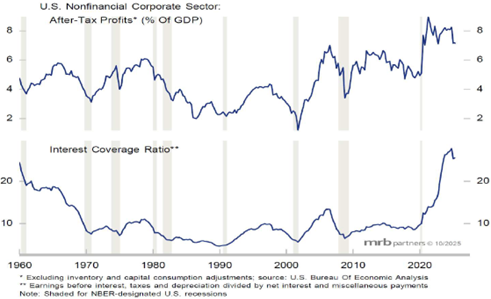

On the corporate side, the picture is decidedly more reassuring. Company margins (Chart 3, top) remain at historically elevated levels, while the Interest Coverage Ratio (Chart 3, bottom) confirms a strong ability to service debt obligations. In short, despite uncertainty related to tariffs and geopolitical tensions, U.S. companies continue to exhibit solid financial fundamentals.

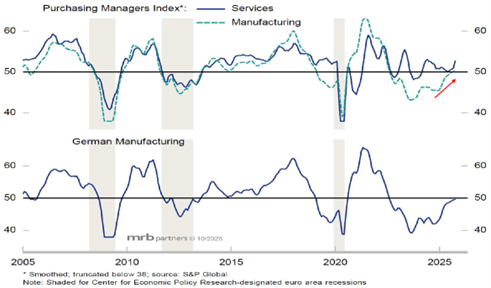

The tone remains constructive in Europe as well. The recovery in the manufacturing sector, driven primarily by Germany, is gaining traction (Chart 4), while wage growth and consumer confidence continue to show resilience. This combination helps to ease some of the concerns that have accumulated in recent years.

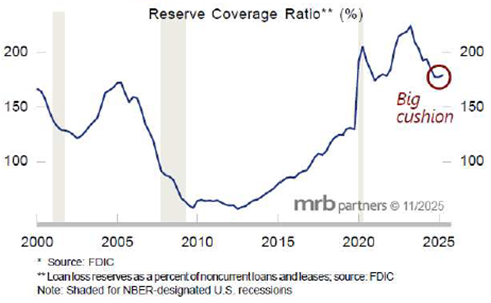

Adding to this resilience is the banking sector, which is likely one of the current strengths of the economic system. The Reserve Coverage Ratio of U.S. banks (Chart 5, bottom) indicates ample reserves relative to expected losses, a cushion large enough to absorb potential shocks. European banks display even stronger metrics, supported by the stricter regulatory framework imposed by the ECB.

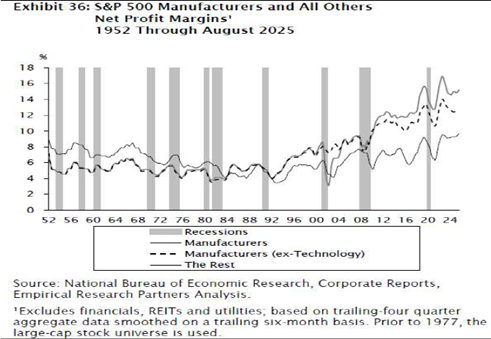

Chart 6 broadens the perspective on corporate margins across all sectors, showing that the improvement has not been limited to technology. In recent years, all major industries have benefited from low interest rates, globalization, tax advantages, and greater energy efficiency. Margin expansion has therefore been broad-based and structural.

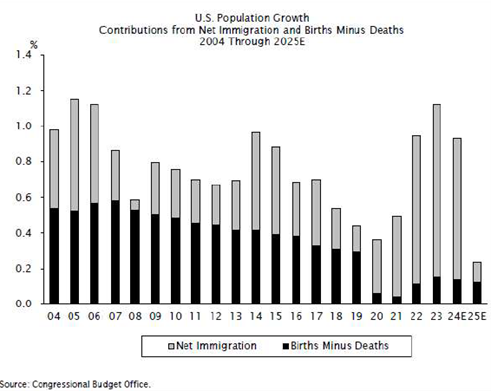

There is, however, a long-term dynamic that could weigh on the cycle in the coming years: demographics. The restrictive stance on illegal immigration adopted by the Trump administration has significantly slowed population growth. Chart 7 shows that overall demographic expansion now stands at around 0.35% per year, less than half the rate observed 15 years ago, with a direct impact on consumption and the housing market.

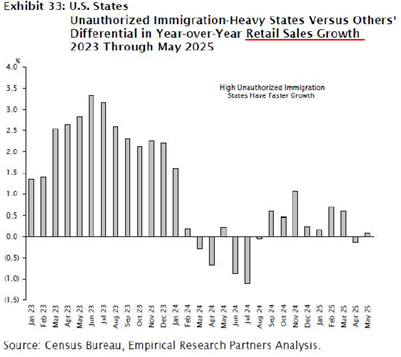

Chart 8 confirms this: in the states most exposed to the decline in immigration, retail sales are weakening, and reduced housing demand is cooling rental prices. This secondary effect is contributing to the slowdown in inflation.

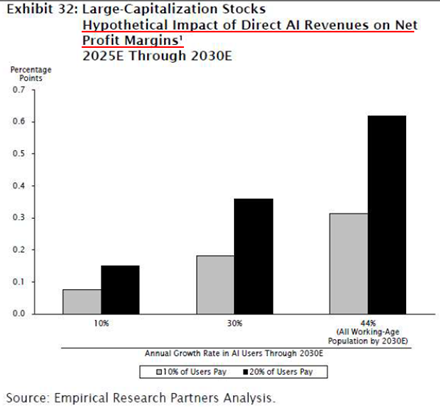

Lastly, technology. According to Empirical Research, artificial intelligence could boost S&P 500 companies’ margins by roughly half a percentage point (Chart 9). This is a positive but modest contribution — not enough, at least for now, to justify on its own the elevated valuations of companies most exposed to the AI theme, especially considering the high costs and still limited revenues generated so far.

PLAYING WITH FIRE

Turning to markets, the key question is: how much of the current environment is already priced in? And, more importantly: are we playing with fire?

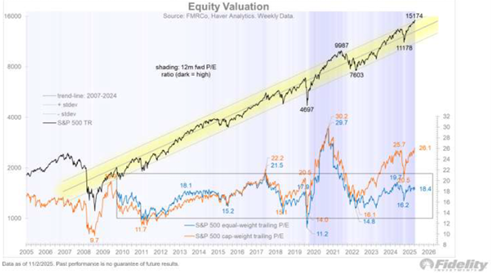

Chart 10 places the current S&P 500 bull market in a historical perspective. The valuation of the cap-weighted index, driven by the major technology names, is elevated (26.1x earnings). The equal-weighted index, on the other hand, while trading at a premium, remains much closer to its average levels of the past twenty years. The message is clear: the market as a whole does not appear excessively overvalued; it is primarily the mega-caps that are. This condition is, however, partly justified by their superior growth, high margins, and strong cash-flow generation in recent years.

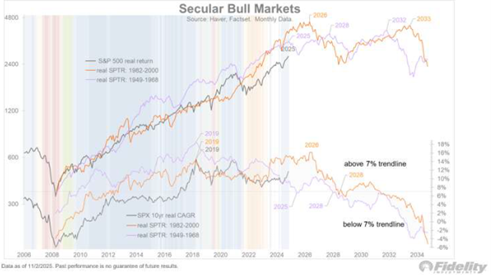

Chart 11 adds an additional layer of analysis by comparing the current cycle with two long-lasting positive cycles of the past (1982–2000 and 1949–1968). If the market were to follow similar trajectories, there could still be room for further gains over the next 12–24 months, supported by a favorable macroeconomic backdrop and ongoing fiscal stimulus.

The main uncertainty remains Artificial Intelligence. Chart 12 shows particularly elevated multiples in the tech sector, which represent the main point of vulnerability should investors’ expectations around AI be revised.

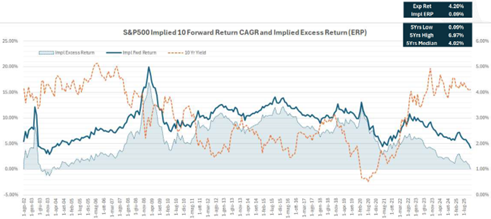

Lastly, as discussed in previous publications, we report the Equity Risk Premium (ERP). Our internal model (Chart 13) indicates an implied ERP of just 0.09%. In other words, the S&P 500 offers an expected annual return of around 4.20% over the next decade—very close to the 10-year Treasury yield (4.11%) but with significantly higher volatility. Yet, despite such a modest risk premium, the macro backdrop and ongoing fiscal policies allow us to maintain a constructive outlook on equities in the near term.

About the author

LFG+ZEST SA